Why insurance support is different

Most "how to automate customer support" advice was written for e-commerce or SaaS, where the worst case is a slightly annoyed customer. Insurance is not that. A wrong answer about a premium is a bad day; a wrong answer that reads as coverage advice can be an unlicensed-advice problem, and a leaked policy record (name, date of birth, policy number, sometimes health data) is a reportable breach.

The thing that makes insurance tricky isn't the volume, it's the line between a fact and a decision. "What's my claim's status?" is a fact your system already knows. "Will my policy cover this?" is a decision that, done wrong, is either bad advice or a regulated act. A support agent, or an AI standing in for one, is allowed to do the first and not the second.

This is the same fine line a legal-tech founder described to us, and it maps onto insurance almost word for word:

"In legal tech you can't afford to get anything wrong, there's a fine line between being helpful and overstepping into legal advice."

Jesse Jenkins, Co-Founder at Willfully (eesel customer)

Swap "legal" for "coverage" and that's the whole insurance challenge in one sentence.

The good news is that the volume problem in insurance support is boringly ordinary. Policyholders ask where to download their ID card, why their premium went up, how to reset their portal password, whether their claim has been processed, and how to add a driver or a dependent. None of that needs a licensed producer, and most of it is textbook ticket classification work. That's the pile you want an AI working through, so your human team has room for the calls that actually need a person, and your SLA targets stop slipping during open enrolment or after a catastrophe event.

What you can safely automate (and what you can't)

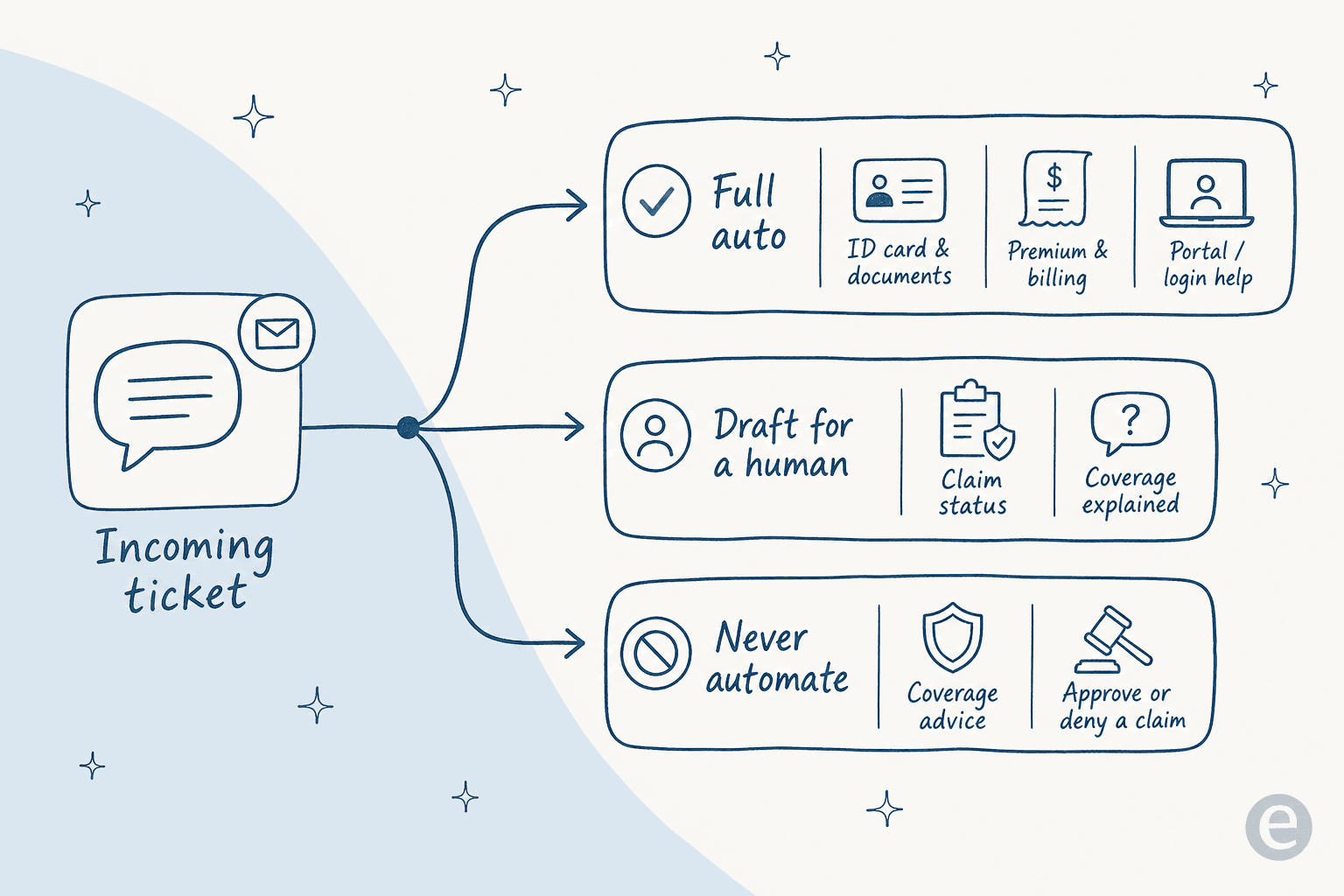

The single most important design decision is drawing the line between what the AI handles and what it never touches. Get this right and the rest is mostly setup.

Here's how I'd split the common insurance ticket types:

| Ticket type | Automate it? | Why |

|---|---|---|

| ID card, policy documents, proof of insurance | Full auto | High volume, pure lookup, no judgement |

| Premium, billing, and payment questions | Full auto | Answers live in your knowledge base and policy docs |

| Portal / password / login help | Full auto | Pure account support, identical to any portal access ticket |

| Claim status ("where is my claim?") | Full auto | A lookup, once the AI can read status safely |

| Coverage explanations (what a term means) | Draft for a human | Often fine, but the wording can shade into advice |

| Policy changes (add a driver, update address) | Draft for a human | Usually routine, but a wrong edit has cost consequences |

| "Will this be covered?" / "Which plan should I buy?" | Never | This is coverage advice. Route to a licensed human |

| Approving, denying, or disputing a claim | Never | A regulated decision, not a support task |

The line that matters most is the bottom two rows. An AI support agent should never recommend coverage, interpret a policy as advice, or approve or deny a claim, full stop. The safe pattern is what one CX lead described perfectly when they were shopping for an AI:

"The AI will never be able to answer 100% of the questions... I need an AI who is only handling the tickets that it's confident to handle and all the other ones, leave them alone."

a CX lead evaluating AI support tools, from an eesel sales call

That's confidence-based routing, and it's the feature that separates a compliance-safe setup from a reckless one. The AI answers what it's sure about and quietly leaves the rest for a person. If a tool can't do that, it doesn't belong anywhere near a policyholder inbox. It's the same control principle behind good ticket triage, AI escalation rules, and a clean AI-to-human handoff in any vertical, just with higher stakes.

Before you automate anything: the compliance gate

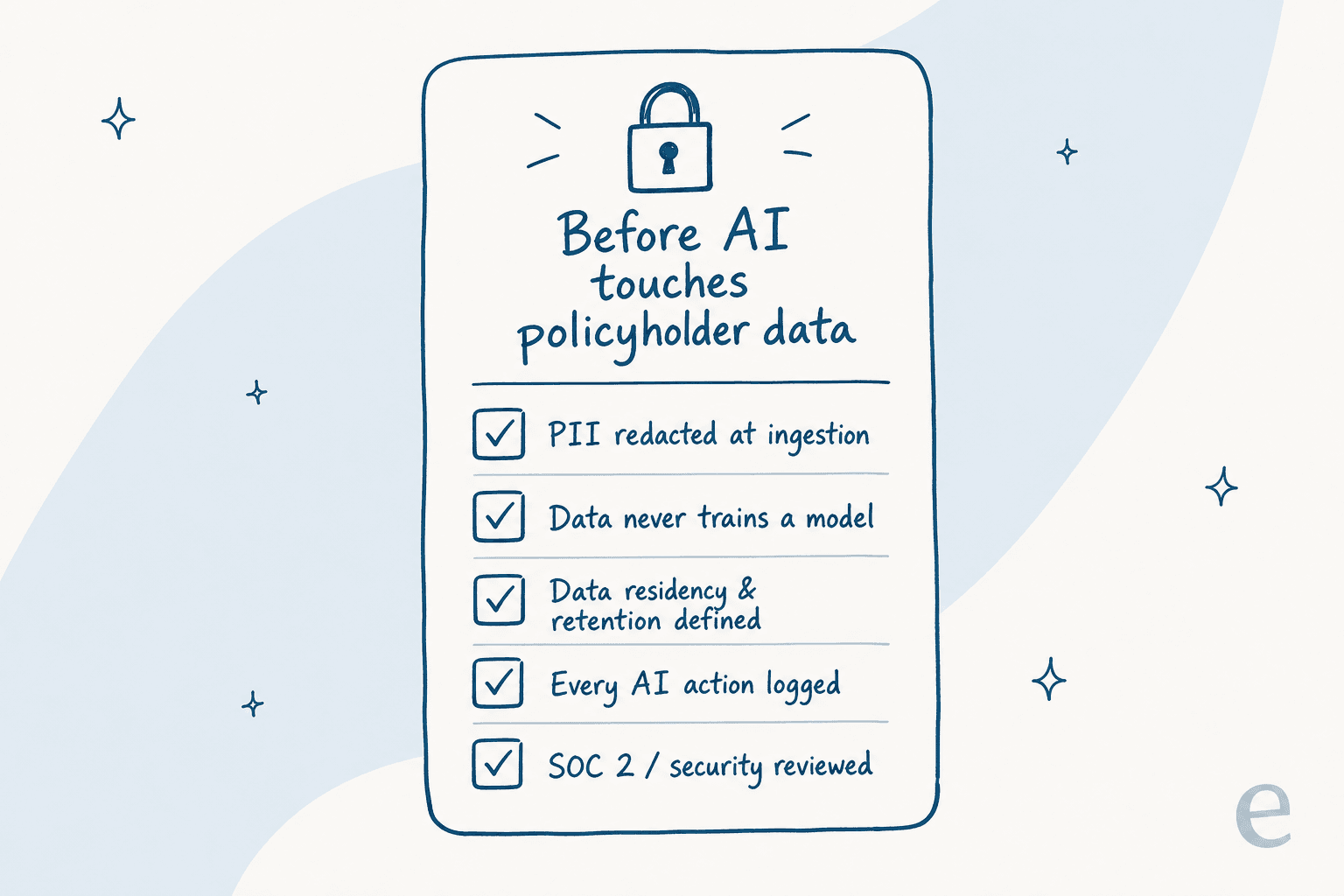

This is the step teams skip, and it's the one that gets a rollout pulled in a regulated industry. Before an AI touches a single policyholder message, you need honest answers to a handful of questions.

- Is PII redacted before storage? Insurance tickets are full of it, names, dates of birth, policy and claim numbers, and for health or life lines, medical detail. The best pattern is redaction at ingestion, so that data is stripped before anything reaches a database or search index. eesel does this at ingestion, so the original data never lands in storage.

- Does your data train the model? The answer you want is a flat no. eesel's is: your data is never used for model training, and the underlying models (Claude, GPT, Gemini) retain data for at most 30 days for abuse monitoring, then it's purged.

- Where does the data live, and how long? Know your hosting region and retention window. eesel runs on AWS with EU hosting available on request and full deletion within 60 days.

- Is every AI action logged? You want an audit trail of what the AI did and why, so a compliance or market-conduct review is a report you pull, not a fire drill.

- For health-adjacent lines, is there a signed BAA? If you handle protected health information (health, some life and disability lines), you need a Business Associate Agreement before any of it flows through an AI. With eesel this lives on the Enterprise plan, alongside the HIPAA-ready controls that regulated buyers ask for.

One honest note, since a fair guide should say it: SOC 2 Type II is a common requirement for insurance buyers, and eesel's is currently underway rather than certified (the report is available under NDA once complete). GDPR compliance, EU data residency, and the no-training guarantee are already in place. Ask every vendor you evaluate the same questions and make them show receipts, the way this buyer did:

"Does it use some kind of other ChatGPT if it doesn't know the answer, and can that be turned off? Does the knowledge stay closed to our org?"

a technical evaluator at a hardware company, from an eesel sales call

How to automate insurance customer support, step by step

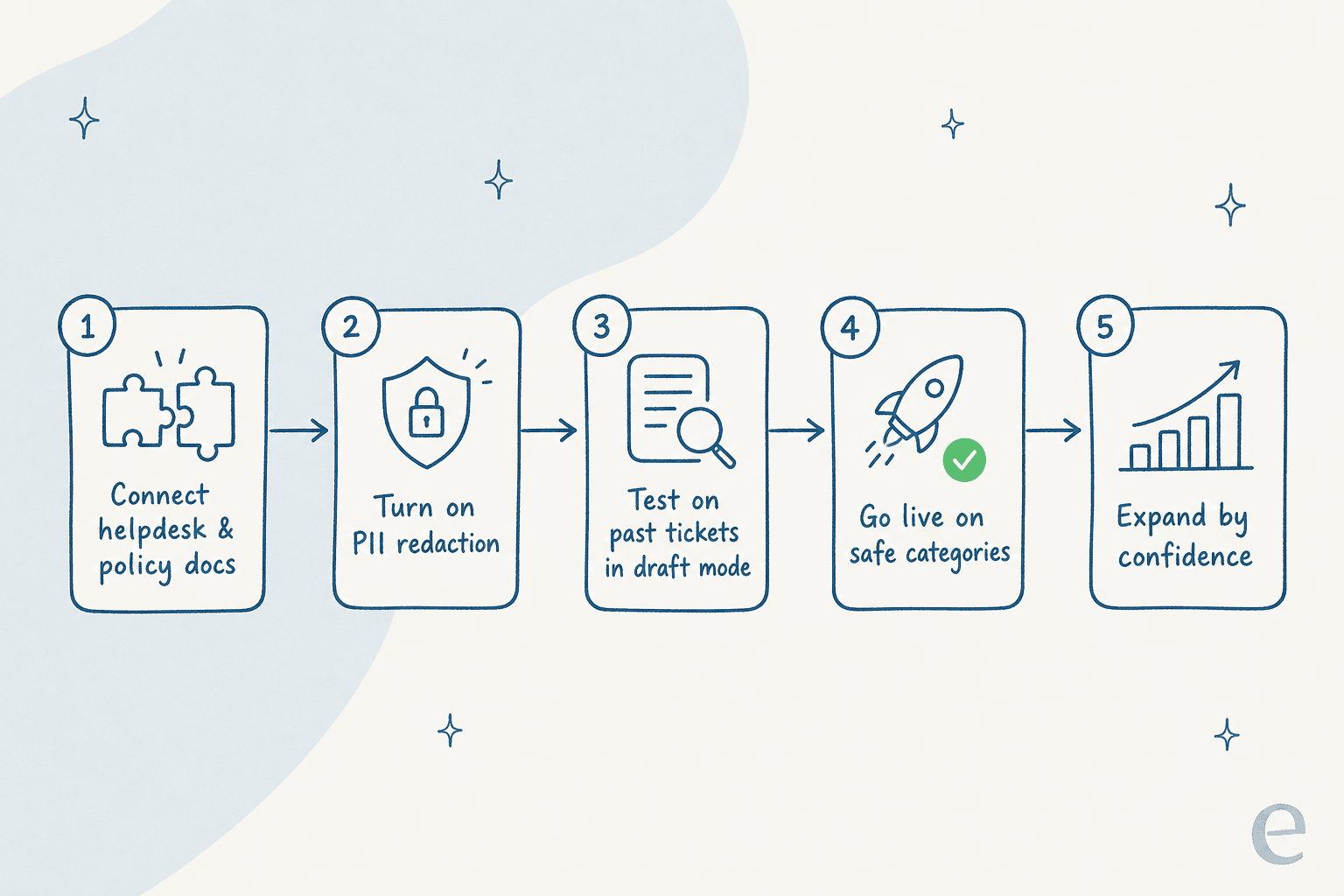

Once the gate is cleared, the rollout itself is fast. The whole point is to move in an order where nothing risky ever reaches a policyholder before you've seen it work.

Step 1: Connect your helpdesk and knowledge

Point the AI at wherever tickets already land (Zendesk, Freshdesk, Front, or a shared email inbox) and at your knowledge sources: help center articles, policy wordings, billing and payment rules, claims FAQs, and past tickets. The AI can only be as accurate as what it reads, so this is where the real work is. eesel connects to over 100 integrations and knowledge sources like Confluence, Notion, and Google Docs.

Step 2: Lock down compliance before it goes anywhere

Turn on PII redaction, sign the BAA if you handle health data, and confirm the retention and residency settings from the gate above. Do this now, not after a pilot, because the moment a real policyholder message flows through an unconfigured tool, you've potentially created the exact exposure you're trying to avoid. This is the non-negotiable step, and it's why insurance rollouts look different from a standard support automation project.

Step 3: Test on your own past tickets, in draft mode

This is the step I'd never skip in insurance. Instead of pointing a fresh AI at live policyholders, run it against tickets you've already resolved and compare its draft answers to what your team actually sent. In draft mode, the AI writes a reply but a human reviews before anything goes out, so a wrong answer is caught in a spreadsheet, not in a customer's inbox. It's the same idea as training AI on your knowledge base, applied as a safety check.

When we ran this kind of cross-validation on a real support inbox, the AI hit 93% triage accuracy and caught 100% of spam with zero false positives across a 284-chat trial. Numbers like that are what tell you which categories are ready.

Step 4: Go live on safe categories only

Turn on full automation for the green-light rows from the table: ID cards and documents, billing, portal access, claim status. Leave coverage explanations and policy changes in draft-only. Leave everything that's a coverage recommendation or a claim decision routed straight to a licensed human. Resist the urge to flip everything on at once, a narrow, reliable rollout builds more trust with your compliance team than a broad, shaky one.

Step 5: Watch the reports and expand by confidence

Once live, the AI keeps learning from resolved tickets, and you watch the reports to see resolution rate by category. When a draft-only category has been correct for weeks, promote it to full auto. When something looks off, tighten the instruction (in plain English, no rebuild) and it applies immediately. Teams that roll out this way commonly resolve a large share of tier-1 tickets inside the first month, one eesel customer reported 73% of tier-1 requests resolved after a seven-day trial.

Common mistakes to avoid

- Letting the AI answer "will this be covered?" No amount of accuracy makes it safe to give coverage advice through a support bot. Route it to a licensed person.

- Turning on claim decisions. Reporting a claim's status is fine; approving, denying, or disputing one is a regulated act. Keep that firmly on the human side.

- Skipping PII redaction. Insurance tickets are dense with personal data. Redact at ingestion before anything is stored, not after.

- Going live without testing on past tickets. You wouldn't put a new agent on a policyholder inbox untrained. Don't do it to an AI either. This is where a lot of AI ticket triage projects quietly fail.

- Picking a tool that can't do confidence routing. If it answers everything or nothing, it's not built for regulated support.

- Ignoring the pricing model. Per-seat tools charge whether the AI resolves anything or not. For a support team weighing AI versus human cost, a usage-based model tracks what you actually get.

Try eesel for insurance support

If you're automating a policyholder inbox, eesel AI is built for exactly the order this guide walks through. It plugs into your existing helpdesk in minutes, redacts PII before storage, offers a BAA on Enterprise for health-adjacent lines, and lets you simulate on past tickets before a single policyholder sees a reply. Confidence-based routing means it handles the ID-card-and-billing pile and hands anything that's a coverage decision to your team, and you only pay for tickets it actually resolves, from $0.40 each.

You can start with the free trial ($50 of usage, no card) or book a demo if you want to walk through the compliance setup with someone first.

Frequently Asked Questions

How do you automate insurance customer support without giving unlicensed advice?

Which insurance support tickets are safe to automate first?

Should an AI ever approve or deny an insurance claim?

How much does it cost to automate insurance customer support?

How do I test AI on insurance tickets before going live?

Article by

Kurnia Kharisma Agung Samiadjie

Kurnia is a software engineer and writer at eesel AI with two years of SEO experience, writing about AI tools, helpdesk software, and customer support. He pairs a developer's understanding of how these products are built with search-driven research into what actually ranks and resonates with the people searching for them.