Conversational AI for insurance: what works, what breaks

Riellvriany Indriawan

Katelin Teen

Last edited July 5, 2026

What conversational AI actually means for insurance

Strip away the marketing and conversational AI is just this: a customer says what they want the way they'd say it to an agent, and the software understands the intent and either answers or does the task. No menu tree, no "press 2 for claims."

There's a sophistication ladder worth knowing, because insurers sit on every rung of it:

- Rule-based chatbots run on decision trees and keywords, so the customer is boxed into predefined buttons. If you've read our take on an AI agent versus a rule-based chatbot, this is the bottom rung.

- NLU chatbots use natural language understanding to catch the intent behind free text, not just keywords.

- LLM-backed agents are the new top rung, and the one everyone means when they say "conversational AI" in 2026.

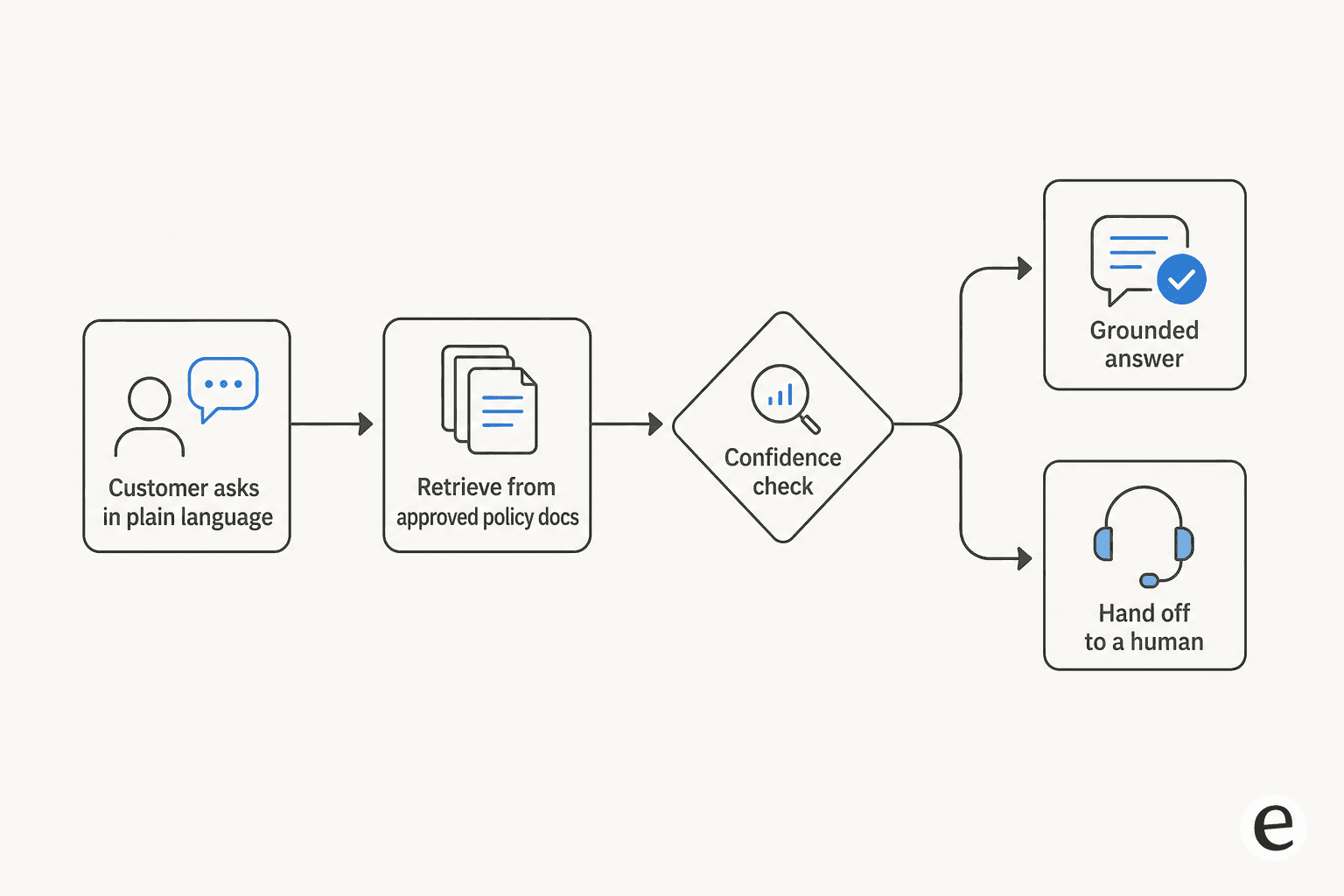

The rung that makes an LLM safe for insurance is retrieval-augmented generation, or grounding: the model answers from the insurer's own policy documents and help center instead of its training weights. That is the difference between an agent that says "your renters policy covers theft up to your limit, here's the clause" and one that cheerfully makes up a number. Our explainer on why chatbots answer incorrectly walks through what goes wrong when that grounding is missing.

Here's the shape of a well-built flow, and why the confidence check in the middle is the load-bearing part:

The ceiling is real, too. Chatbots are great at basic inquiries and fall apart as the problem gets complex, which is not a knock on the tech, it's the design brief. The tools people like are the ones that know their own limits and reach for a person. Our overview of AI in customer service covers that boundary in general terms; insurance just raises the stakes on getting it wrong.

Where it's already working: real insurer deployments

The proof isn't in a vendor deck, it's in the insurers' own numbers. Here are the flagship deployments, all sourced from primary company material:

| Insurer | Assistant | What it handles | Published number | Line |

|---|---|---|---|---|

| Lemonade | AI Maya, AI Jim | Quotes, FNOL, claims triage, fraud flagging | ~55% of claims automated, 96% of FNOL no-human (10-K) | Home, renters, pet |

| GEICO | Virtual Assistant | Policy coverages, billing, ID cards, 24/7 | Not published | Auto |

| Progressive | Flo Chatbot | Auto quotes, Q&A, human hand-off | First top-10 US insurer to quote in Messenger (2017) | Auto |

| Aetna (CVS Health) | AI navigation | Benefits nav, prior-auth, find-a-doctor, costs | Serves ~37M members; voice in 2026 | Health |

| Cigna | Virtual Assistant | Check coverage, estimate costs, find care | Launched June 2025 | Health |

The most documented case is Lemonade. Its claims bot, AI Jim, once paid a stolen-coat claim in three seconds flat: it reviewed the claim, cross-referenced the policy, ran 18 anti-fraud algorithms, approved it, wired $729, and told the customer, all between 5:49:07 and 5:49:10 on a December morning in 2016.

Here's the part that matters most, and it's Lemonade's own statement: it has never let AI auto-reject a claim. The bot does the fast approvals and the fraud-flagging; anything it flags goes to a human investigator. The AI automates the easy "yes" and escalates the hard "no." That single design choice is the difference between the deployments that win awards and the ones that end up in a regulator's inbox.

On the health side the pattern is servicing, not claims decisions. Aetna is embedding generative AI across its app so members can ask "does my x-ray require approval?" without knowing the words "prior authorization," and Cigna built its assistant around a blunt stat it published: 4 out of 5 US adults don't feel confident about their own health benefits. Plain-language coverage answers are exactly the kind of high-volume, low-risk work these agents are good at, and it maps closely to AI customer service for insurance more broadly.

What policyholders actually think

Here's the part vendor pages skip. If you read where real customers talk, the frustration voice is louder and more specific than the praise, and it's worth listening to because it tells you exactly what to avoid.

The angriest complaint is the loop that won't escalate, especially when a claim is on the line:

"I cannot imagine navigating a claim without the ability to talk with a human being. Home insurance is not the place to cheap out!"

That instinct shows up across every auto and health thread too: people want a visible human, and trust drops the moment money or a dispute is involved. An insurance rep watching bots land in their queue put the technical limit plainly:

"AI bots can sometimes get basic benefits or claim info if the system is straightforward, but they usually hit a wall with anything complex"

None of this says "don't." The praise is just as real when the tool respects the line, as the industry reaction to Lemonade's speed showed:

"Settling a claim in two seconds is by no doubt impressive, and just goes to show the effectiveness of deploying generative AI in business"

And practitioners who've shipped these agree the human doesn't disappear, it moves up the value chain. As one insurtech operator, Michael Rudman, founder and CTO at Jones, put it on LinkedIn: "The better AI gets, the more valuable human conversations become." Getting the handoff right is what separates the deployments people tolerate from the ones they rage-quit.

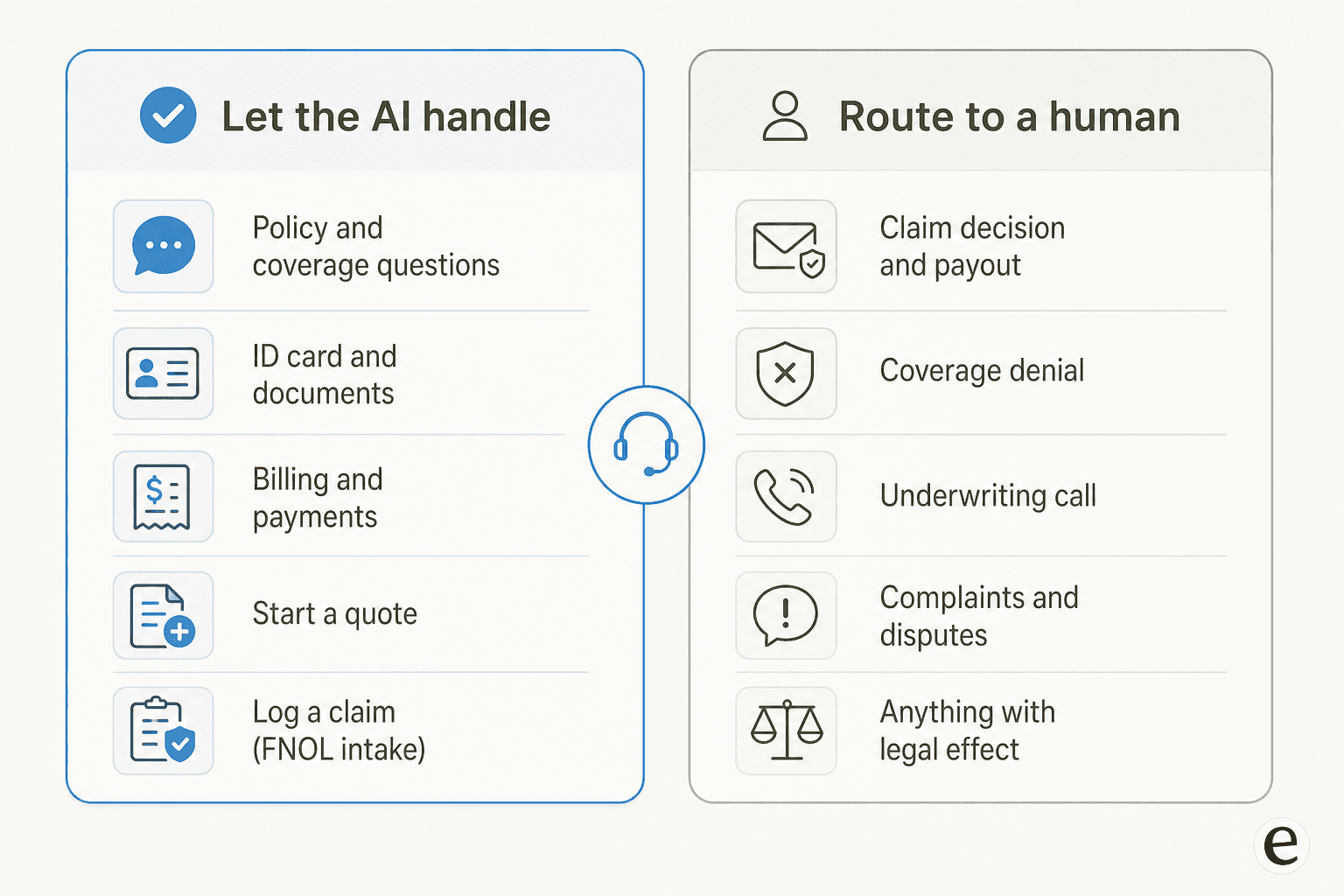

What to automate, and what to send to a human

So where's the line? After watching a lot of these go live, my rule is simple: automate the lookup, escalate the decision. If answering the question could deny a claim, change coverage, or invoke a legal right, a human owns it. Everything else is fair game for the agent.

The left column is where the volume and the savings live, and it's exactly the tier-1 work that eats an insurance support team's day. It maps cleanly to what a good AI helpdesk agent already does well: deflect the repetitive stuff, keep answers consistent, log everything. The right column is where a wrong answer becomes a regulatory problem, so those flows should capture the intent, then route, never guess.

The mistake I see most is teams pushing the line rightward too fast, letting the bot attempt claim decisions or coverage calls because a demo made it look capable. That's how you end up in the angry threads above. Start narrow, prove it on the left column, and expand only when your deflection rate and your escalation quality both hold up. Lemonade's own split, automating approvals while a human owns every rejection, is the template.

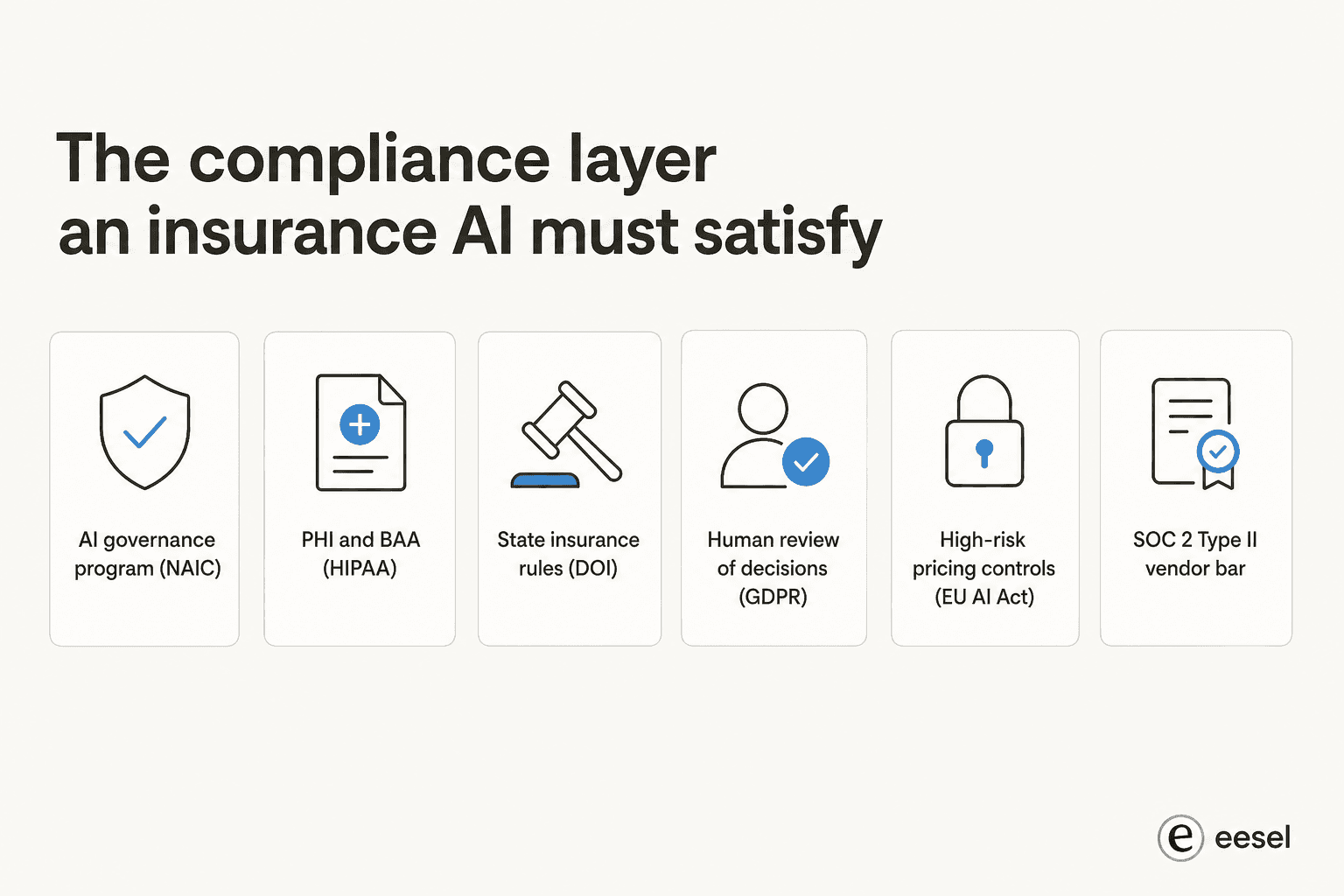

The compliance layer insurance adds

This is what makes insurance different from generic support. A wrong answer here isn't just an annoyed customer, it's a regulated carrier potentially breaking the law. So an insurance bot carries a compliance surface a generic support bot doesn't:

Walking the stack:

- AI governance (NAIC). The NAIC AI Model Bulletin, adopted in December 2023 and by 24 states as of August 2025, tells insurers to run a written AI Systems program covering governance, risk controls, and vendor oversight. Crucially, it holds you accountable for AI you buy from a vendor, not just AI you build.

- Automated claims are still claims. The bulletin is blunt: actions must not violate the Unfair Claims Settlement Practices Act "regardless of the methods" used to make them. Automation is no defense to an unfair-claims complaint.

- State rules. Colorado's Regulation 10-1-1 demands a governance framework for predictive models, and New York's Circular Letter No. 7 sets an unfair-discrimination test for AI in underwriting and pricing.

- Health data (HIPAA). Health insurers are covered entities, so any AI vendor touching protected health information needs a signed Business Associate Agreement before it processes a single record.

- Human review (GDPR and the EU AI Act). For EU customers, GDPR Article 22 gives a right not to be subject to a solely automated decision with legal effect, plus a right to human intervention. And the EU AI Act's Annex III classes AI for "risk assessment and pricing in relation to natural persons in the case of life and health insurance" as high-risk, which triggers logging and human-oversight duties.

- The vendor bar. Carriers buying a tool will expect a SOC 2 Type II report, which tests that controls actually operated over time, not just that they exist on paper.

The through-line across all of it is the same design pattern policyholders were begging for: grounding, logging, and a human off-ramp. Three separate frameworks independently mandate that escalation path. If you're evaluating tools, our note on AI knowledge management for support teams covers keeping that approved-knowledge layer clean, which is where accuracy starts.

How to deploy conversational AI without the horror stories

Put the customer voice and the compliance surface together and the playbook is clear. Here's what I'd do, in order.

Ground everything, then prove it before go-live. Restricting the agent to your approved policy docs and help center is what keeps it from inventing a coverage limit. But grounding alone isn't proof, so the real safeguard is simulating the agent against thousands of your real past tickets first, so you see where it would have hallucinated before a customer does. This is the step most teams skip, and it's the one that catches the wrong-answer risk while it's still free.

Gate on confidence and keep the human visible. Set a threshold: below it, the agent drafts for a human or hands off rather than replying live. Cap repeat attempts so you never build a loop. The single most-requested feature in insurance-bot feedback is seamless escalation, and it's exactly what the angry threads above were denied.

Keep sensitive data where it belongs. When we onboard finance and healthcare teams, the hard gate is always data handling. I've sat in on reviews where a buyer needed assurance that ticket data with policy and payment details stayed in their environment; the honest answer is that the agent should reason over question type and response style, with custom retention and PII redaction, and no customer data used to train models. Those are the questions your security review should be asking any vendor, especially with HIPAA in play.

Start on tier-1, expand on evidence. The realistic scope, echoed by operators over and over, is tier-1 deflection: let the agent own the "what does my policy cover" and "where's my ID card" questions that eat support time, and route the messy stuff to a person. Expand only when your first-contact resolution holds. If it feels slow, that's the point, this is one place where AI versus human support is a partnership, not a replacement.

Try eesel for insurance support

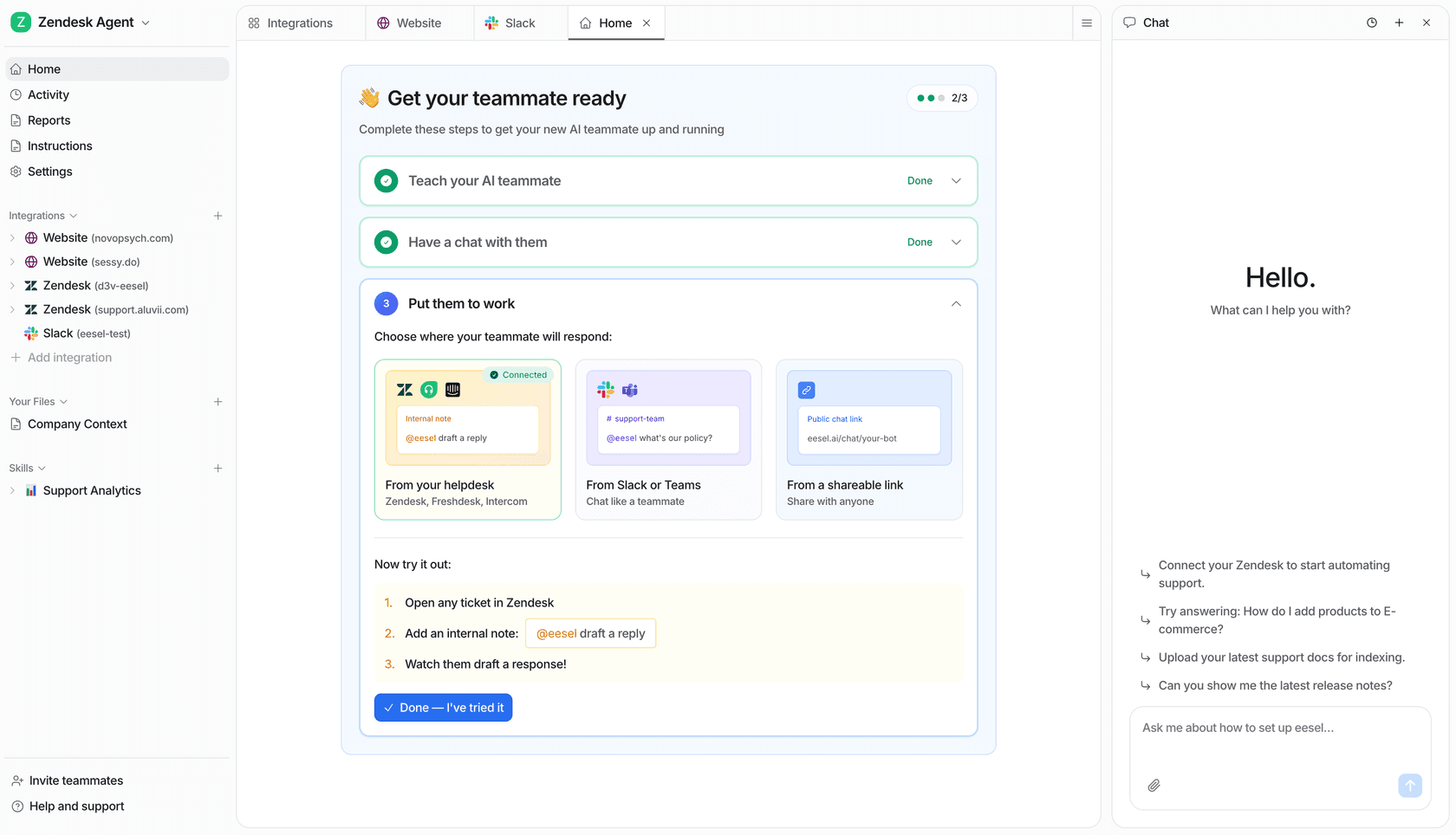

If you're a carrier, an MGA, or an insurtech weighing this up, eesel is built for exactly the pattern above. It plugs into the helpdesk you already run, learns from your past tickets and policy docs, and answers only from that approved knowledge, so it deflects the tier-1 lookups without wandering off-script into a coverage promise you never made.

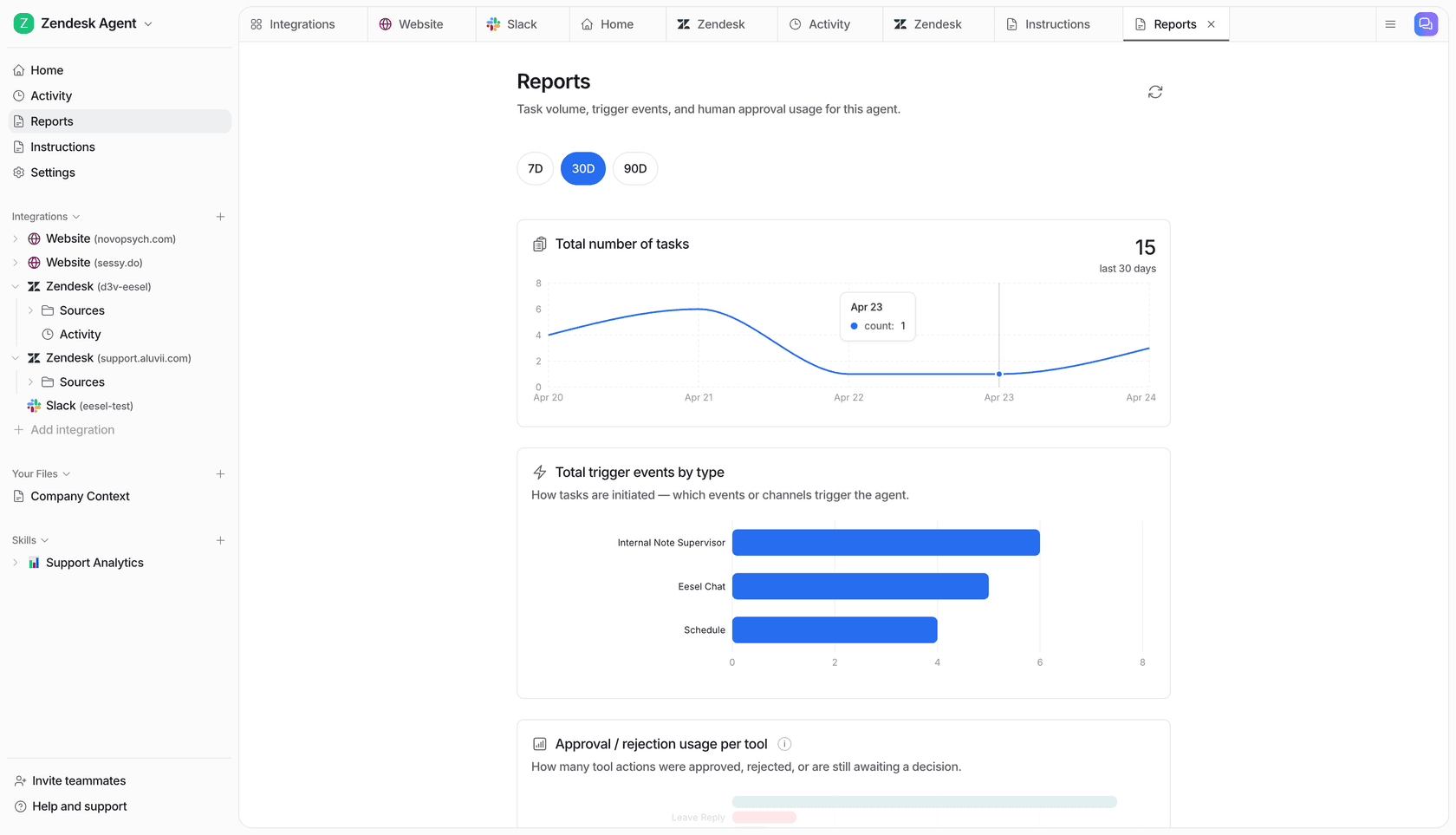

The part that matters most for a regulated team: you can simulate the agent against thousands of your real historical tickets before it replies to a single live customer, then turn on autonomy gradually with confidence-based routing and a clean human handoff, the same automate-the-yes, escalate-the-no split that works for Lemonade. On the compliance side there's SOC 2, GDPR and EU data residency, and PII redaction, and pricing is usage-based at about $0.40 per resolved ticket with no per-seat fees, so you're not paying for a platform you're still testing.

You can try eesel free, or book a demo if you want to walk through the compliance and simulation setup with someone first.

Frequently Asked Questions

What is conversational AI for insurance?

Is conversational AI for insurance safe and compliant?

How much does conversational AI for insurance cost?

What insurance tasks should a chatbot handle versus a human?

What rules apply to conversational AI for insurance?

Article by

Riellvriany Indriawan

Riell is a designer and writer at eesel AI with about two years of experience researching CX platforms, AI chatbots, and helpdesk software. She combines her design background with a sharp eye for how these tools actually look and feel in practice — making her comparisons unusually visual and user-focused.