AI chatbot for banking: what works, what breaks in 2026

Alicia Kirana Utomo

Katelin Teen

Last edited July 4, 2026

What an "AI chatbot for banking" actually means

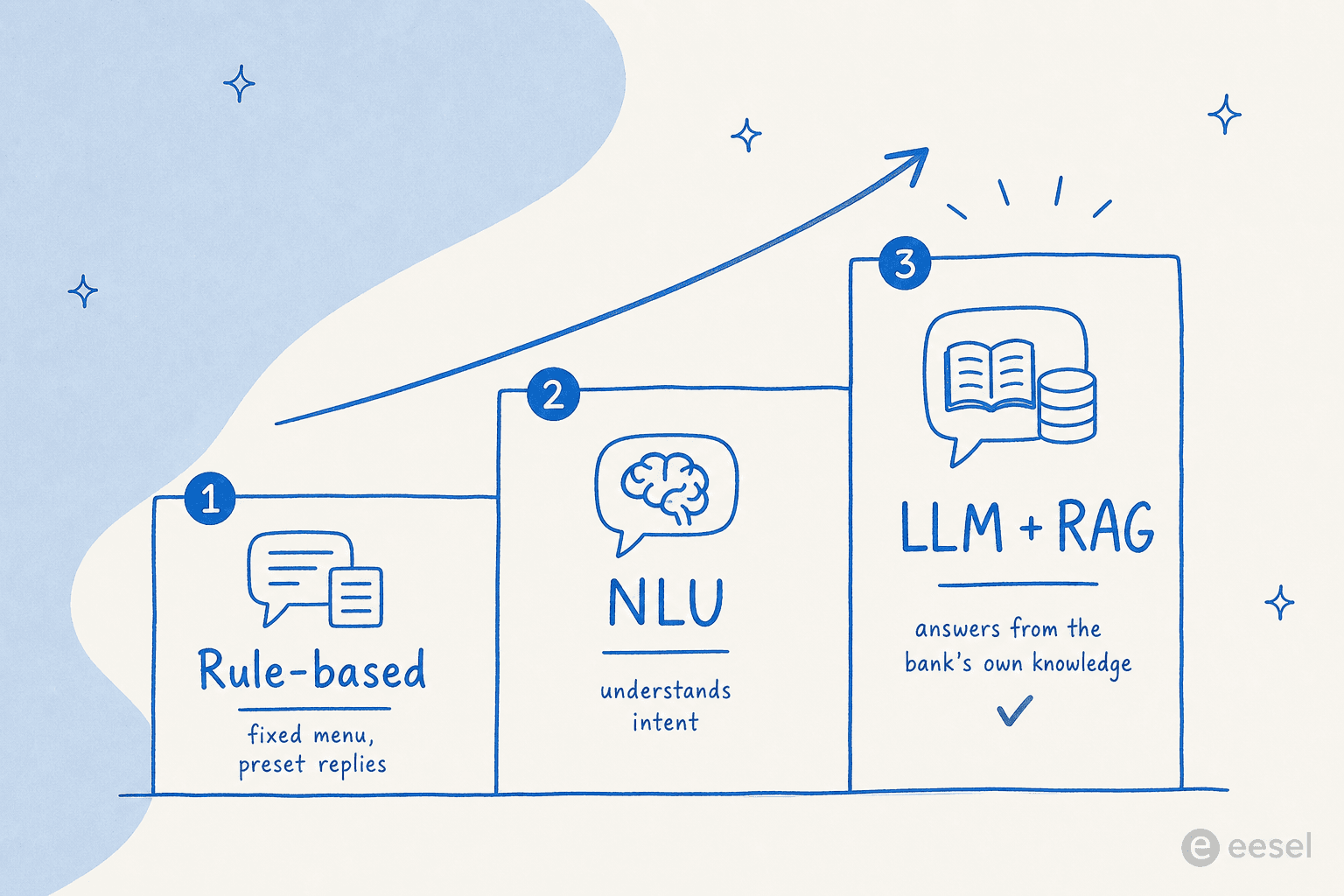

The phrase covers three very different things, and the difference is the whole story. I build support AI for a living, so let me be precise about the ladder, because a bank buying at the wrong rung is where most of the horror stories start.

The US Consumer Financial Protection Bureau's June 2023 report frames it as a sophistication ladder, and the distinctions matter:

- Rule-based chatbots use "either decision tree logic or a database of keywords to trigger preset, limited responses," per the CFPB report. The user picks from a fixed menu ("check balance", "make a payment"). This is the old-school rule-based chatbot, and it's where the "dumb bot" reputation comes from.

- NLU / machine-learning bots use natural language processing to recognise the intent behind free text, rather than matching keywords. NatWest describes its Cora assistant as answering "banking queries 24/7 through natural language processing and machine learning capabilities" (NatWest Group).

- LLM-backed agents with RAG are the newest rung. The CFPB notes banks "moving from simple, rule-based chatbots towards more sophisticated technologies such as large language models." The load-bearing word is RAG (retrieval-augmented generation): the model answers from the bank's own knowledge base, not its training weights. DBS describes its DBS Joy agent as one that "integrates large language models with the bank's proprietary knowledge base," letting it "move beyond pre-programmed static answers to dynamic responses" (DBS).

That RAG grounding is the difference between a chatbot that helps and one that confidently invents an answer about your money. If you only remember one thing from the mechanism, remember that: an ungrounded LLM in a bank is a hazard, and a knowledge-base-grounded one is a tool. It's also why the generic conversational AI pitch and the reality of a safe banking deployment are so far apart.

What banks actually use them for

Enough theory. Here's what the named, live deployments actually do, pulled from the banks' own newsrooms rather than a vendor deck.

Bank of America's Erica, launched in 2018, has assisted nearly 50 million users across more than 3 billion interactions, now averaging over 58 million interactions a month, and BofA says users find what they need over 98% of the time, which "significantly decreases call center volume." Wells Fargo's Fargo hit more than 1 billion interactions in under three years, and notably, more than 3 million Spanish-speaking customers have used it over 160 million times, which tells you multilingual coverage isn't a nice-to-have at scale.

Here's how the marquee deployments line up:

| Bank / bot | Launched | Scale | Named use cases | Build or buy |

|---|---|---|---|---|

| Bank of America - Erica | 2018 | 3B+ interactions, ~50M users | Balance-trend alerts, spending insights, rewards, appointment scheduling with human handoff | Blend (in-house core) |

| Wells Fargo - Fargo | 2023 | 1B+ interactions | Zelle payments, bill pay, routing numbers, balances | Buy (Google Cloud LLMs) |

| Capital One - Eno | 2017 | SMS-first | Fraud/unusual-charge alerts, card lock/replace, virtual card numbers, declines | Build in-house |

| NatWest - Cora / Cora+ | 2017 | 10.8M queries in 2023 | Cancel a transaction, statements, new card, ISA, mortgage guidance | Buy (built with IBM) |

| DBS - DBS Joy | 2018 / 2025 relaunch | 120k+ chats, CSAT +23% | Corporate/SME FAQs and requests, human handoff | Build in-house |

Map that back to the use cases people actually search for and you get a clean list: balance and transaction queries (Erica, Fargo, Eno), card freeze and fraud alerts (Eno proactively "alerts customers when it spots something unusual, such as a double charge... or potential fraud", per Capital One), payment help (Fargo via Zelle), loan and mortgage guidance (NatWest's Cora+ can now "understand the context and nuances of each query" instead of dumping a link), and financial insights (Erica's balance-trend alerts). These are the same buckets any customer service chatbot handles, just with real money and real regulators attached.

One number worth internalising for the business case: all of the top 10 US commercial banks already run a chatbot, and roughly 37% of the US population (over 98 million users) interacted with one in 2022. This isn't an experiment anymore. If you're evaluating tools, our roundups of companies using AI for customer service and the best AI chatbot for customer service are a useful starting map.

Why banking is different: a wrong answer can break the law

This is the part generic "AI for support" content skips, and it's the part that should shape every build decision. In most industries, a chatbot that gives a wrong answer creates an annoyed customer. In banking, it can create a regulated institution that violated federal law.

The single most important source here is the CFPB's June 2023 issue spotlight. CFPB Director Rohit Chopra put it about as plainly as a regulator can: "A poorly deployed chatbot can lead to customer frustration, reduced trust, and even violations of the law." The report names three risk buckets: noncompliance with consumer-finance law, the now-famous "doom loops" of repetitive jargon with no offramp to a human, and direct consumer harm when bad guidance triggers fees or the wrong product. It even flags that a bot may fail to recognise when a customer is raising a dispute, which is a legally required function.

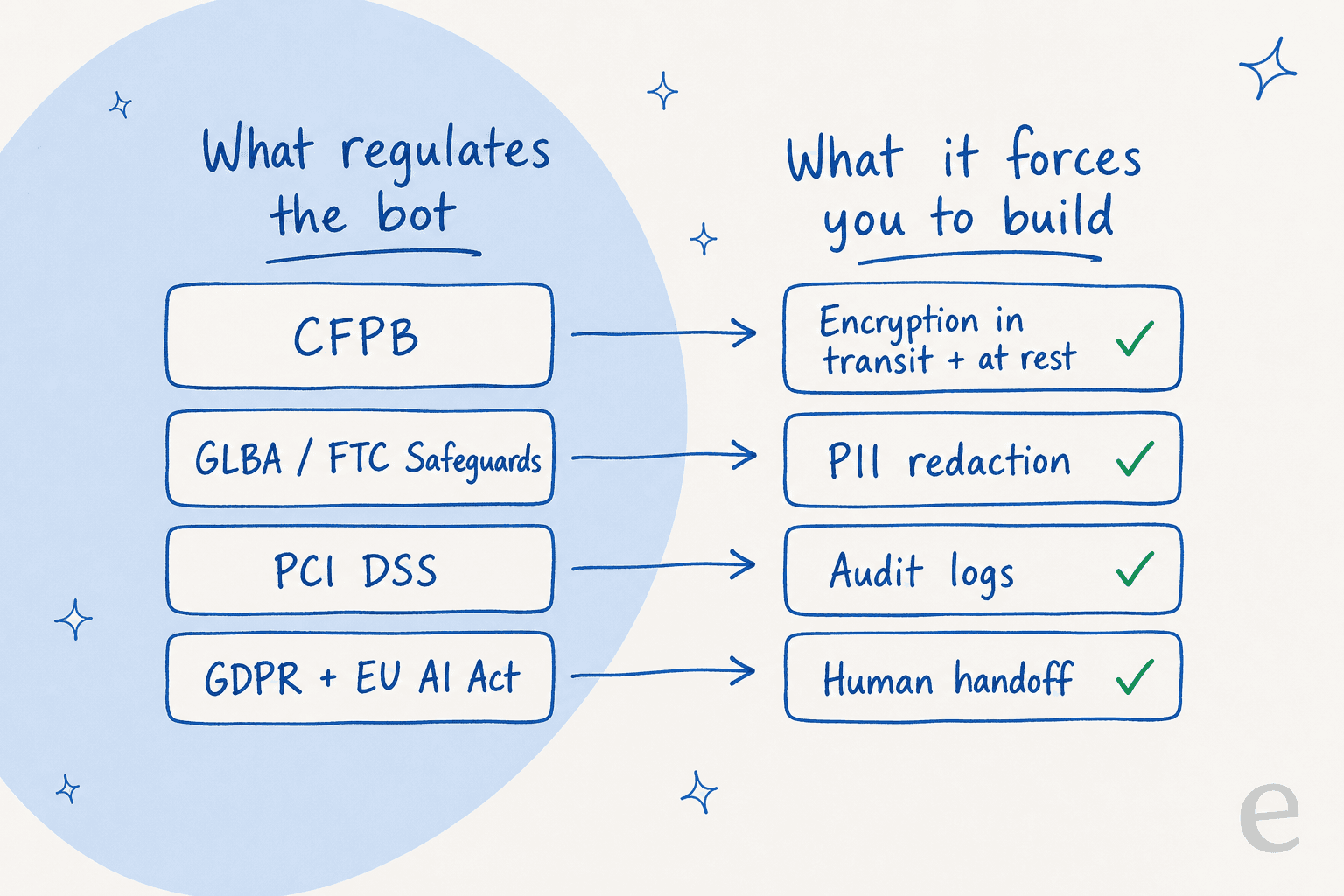

That's the tip of the compliance surface. Depending on where you operate and what the bot touches, you're also standing on:

- GLBA / the FTC Safeguards Rule, which requires encryption of customer information in transit and at rest and, since a 2023 amendment, notifying the FTC within 30 days of a breach affecting 500+ consumers.

- PCI DSS, the moment a flow can surface a card number: the PAN must be masked on display and rendered unreadable at rest. This is why PII redaction in transcripts isn't optional.

- GDPR Article 22 for EU customers, which grants a right not to be subject to solely automated decisions with legal effect (a loan denial is the textbook example) and a right to human intervention.

- The EU AI Act, which classifies AI used to evaluate creditworthiness as high-risk, triggering obligations around logging, human oversight, and accuracy.

Here's the nuance worth stating clearly: a plain support bot answering "what's my balance" isn't automatically high-risk. The trigger is the credit-scoring use case. But the general obligations, telling the customer they're talking to AI, logging everything, keeping a human in the loop, shape any bank deployment. Notice that human escalation isn't a nice-to-have here, it's written into three separate legal frameworks (the CFPB's doom-loop warning, GDPR Article 22, and EU AI Act Article 14). If your vendor treats escalation as an afterthought, walk away.

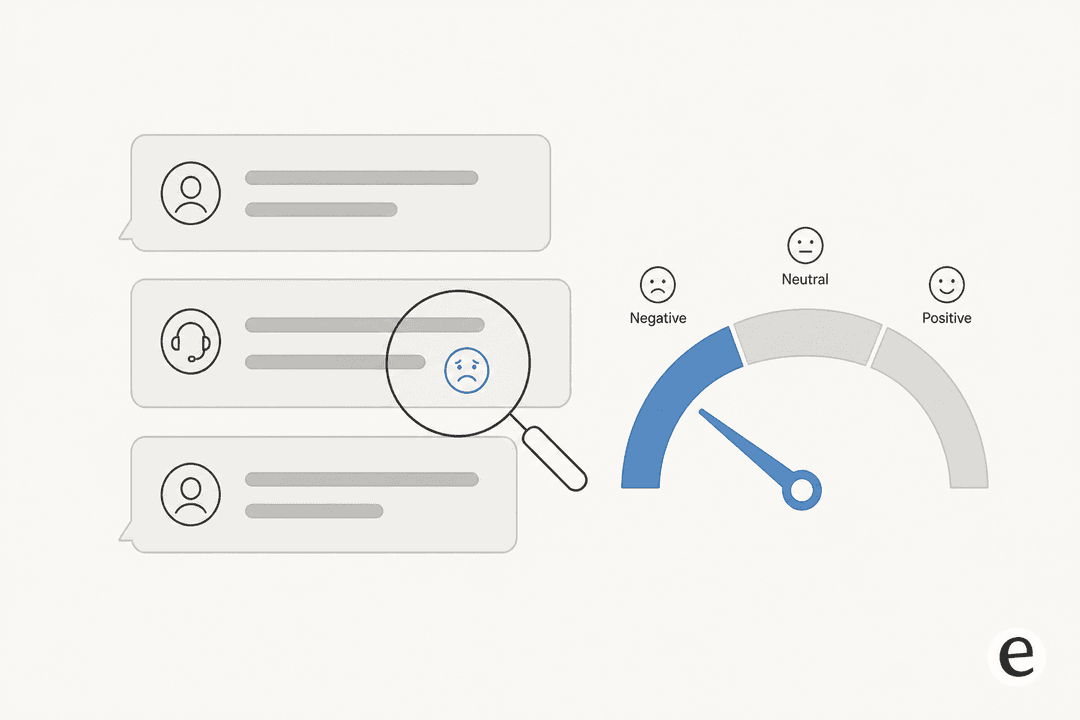

What customers actually think (it's not pretty)

I read a lot of support forums for this job, and the banking chatbot threads are some of the angriest. That's worth sitting with, because it's the flip side of those glossy interaction counts. The recurring complaint isn't "AI is bad", it's "the bot loops and won't let me reach a human, especially when money is on the line."

"I've had fraud happening on my card this week and I've never had such an excruciating experience with a bank... I had to threaten to reach out to KiFid [the Dutch financial ombudsman] for them to allow me to speak to a human. Also the AI will occasionally pretend to be a person too. It's all horrible."

Bitterboule80, r/bunq

The trust collapse is sharpest exactly where banking lives, which one practitioner watching customers summed up neatly:

"i've seen customers be fine with bots for simple stuff but get wary as soon as money or disputes are involved."

thepillowco, r/fintech

And there's a banking-specific flavour of complaint I hadn't fully appreciated until I dug in: the bot as a downgrade of a feature customers already had. On the Bank of America subreddit, one user's rant about Erica wasn't about accuracy at all:

"I NEED A STRAIGHTFORWARD STATEMENT OF MY DEPOSITS. Why do they think we care that we're now asking Erica instead of just filtering the information for what we need to see?"

FamBamJam78, r/BankOfAmerica

The lesson I take from these: an AI chatbot for banking earns its place by removing friction on tier-1 questions, not by inserting itself between a frightened customer and a human during a fraud case. Get that boundary wrong and you don't just annoy people, you lose them to a competitor. Practitioners who deploy these successfully keep landing on the same recipe: rules-based or tightly domain-scoped for regulated flows, LLMs treated with caution, and seamless handover as non-negotiable.

What makes a banking bot actually work

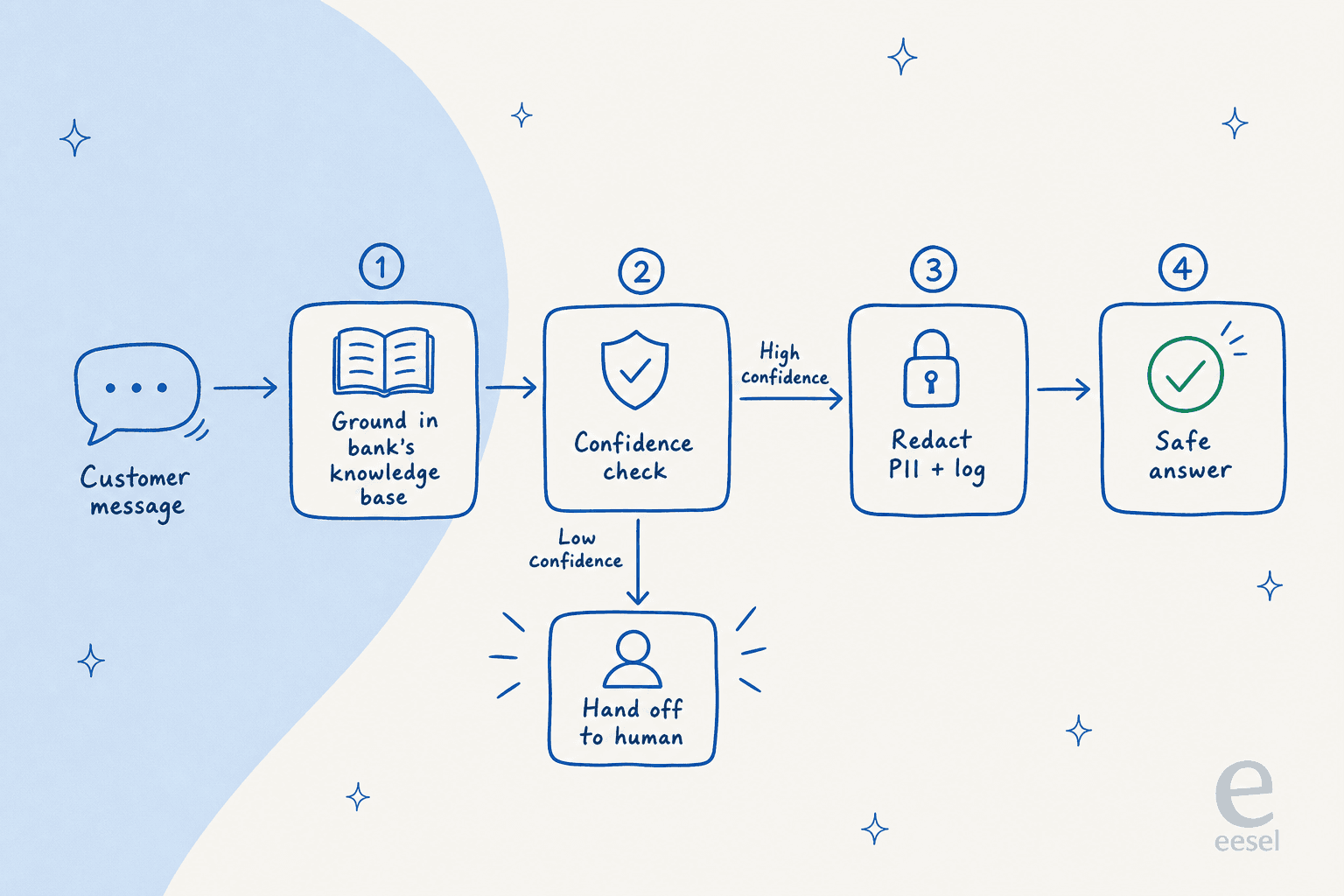

So how do you build one that lands on the right side of all that? After years of putting AI on live support queues, the pattern that holds up in production comes down to four gates every customer message passes through.

- Ground every answer in the bank's own knowledge base. RAG over your verified help center and policy docs, never the open model. The CFPB found chatbots "are ill-suited for tasks that require logic, specialized knowledge, or current data", and grounding is how you close that gap. This is also the single best defence against hallucinations.

- Route on confidence. When the model isn't sure, it drafts for a human instead of sending, or escalates outright. That one behaviour satisfies the human-intervention requirement in GDPR Article 22 and EU AI Act Article 14 at the same time, and it's the difference between a helpful bot and a doom loop.

- Redact PII and log everything. Strip card numbers, SSNs, and account details before anything hits the model, and keep an audit trail. That's PCI DSS and the EU AI Act's record-keeping rules, handled at the plumbing layer.

- Simulate before you go live. This is the one I'd never ship without. Run the bot against thousands of your real historical tickets and see exactly where it would have hallucinated, before a single customer is exposed to it.

That last step is the hard-won lesson. I've watched a confident-sounding bot quietly give wrong answers in testing, which is why I now treat "simulate against historical tickets first" as table stakes rather than a feature. It maps directly onto the CFPB's core concern: test before you deploy. It's also the thing most conversational AI tools quietly skip, because it's uncomfortable to show a buyer the coverage gaps up front.

How to deploy one without getting burned

A few practical calls I'd make if I were standing up an AI chatbot for a bank or fintech today:

- Scope it to tier-1 first. The realistic win is tier-1 deflection, the "what are the fees / how do I withdraw / where's my routing number" volume, not full replacement. One fintech operator put it well: the bot "captures customer intent and routes the messy disputes to humans so people still talk to a person when it matters." Measure it with real customer service KPIs, not a vanity deflection number.

- Buy the layer, don't rebuild the bank. The named deployments split cleanly: Capital One and DBS built in-house, while Wells Fargo, NatWest, and Truist bought or partnered. Unless you have a large ML org, the pragmatic path is an AI layer that sits on your existing helpdesk and learns from your tickets, rather than a multi-year in-house build.

- Interrogate the vendor's security posture. Encryption at rest and in transit, PII redaction, EU data residency, SOC 2, and a clear "your data never trains our models" stance are the baseline. A vendor that can't answer these fast isn't ready for a regulated buyer.

- Wire the handoff before the automation. Design the escalation path first, then automate on top of it. The complaints above are almost all handoff failures, not accuracy failures.

If you want the wider context on tooling, our guides to the best AI chatbot platforms and AI customer service software go deeper, and AI agent vs human agent cost helps size the business case.

Try eesel AI for banking support

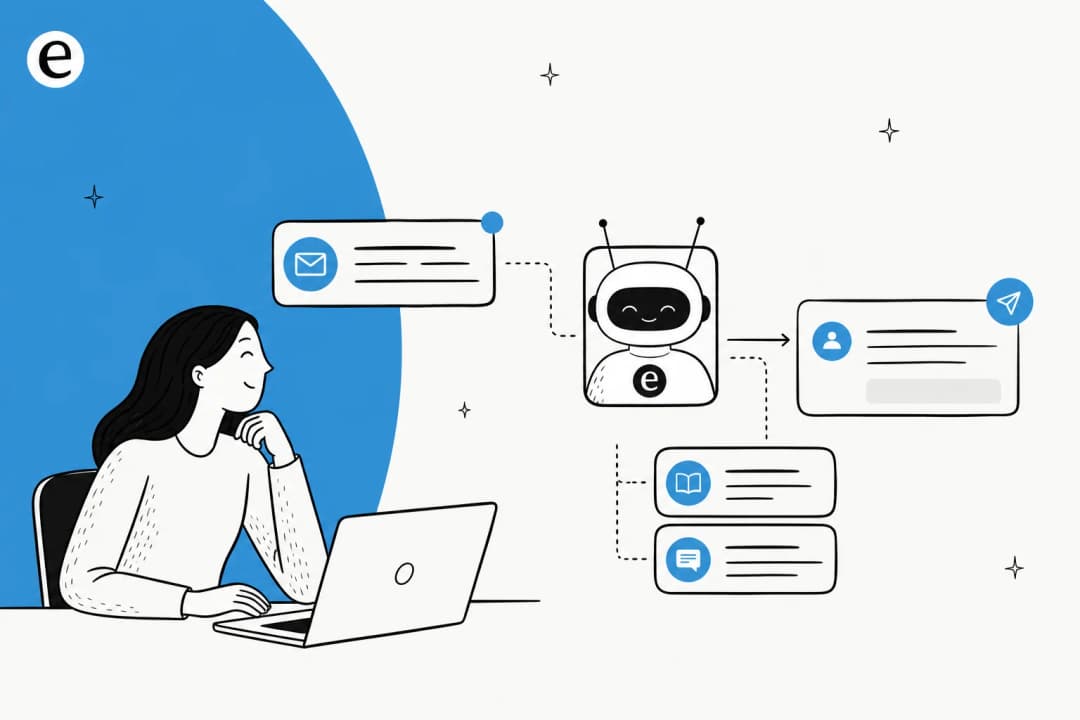

If you're evaluating an AI chatbot for a bank, credit union, or fintech, eesel AI is built around exactly the guardrails above. It plugs into your existing helpdesk (Zendesk, Freshdesk, Front, and more) and learns from your past tickets and help docs on day one, so answers are grounded in your verified content rather than a generic model.

The differentiator for a regulated buyer is the simulation mode: before anything touches a live customer, you replay the agent against thousands of your historical tickets to see coverage and catch where it would have gone wrong. Pair that with confidence-based routing, optional PII redaction at ingestion, AES-256 encryption, GDPR compliance, and EU hosting on request (details on the security page), and you get an AI teammate you can actually put in front of an auditor. It's usage-based at $0.40 per resolved ticket with no per-seat fees, and there's a free trial so you can run a simulation on your own data before committing.

Here's eesel working inside a live helpdesk:

Frequently Asked Questions

What is an AI chatbot for banking?

Is an AI chatbot for banking safe and compliant?

How much does a banking chatbot save?

Can an AI chatbot for banking handle disputes and fraud?

What is the best AI chatbot for a bank's support team?

Article by

Alicia Kirana Utomo

Kira is a writer at eesel AI with a Computer Science background and over a year of hands-on experience evaluating AI-powered customer service tools. She focuses on breaking down how helpdesk platforms and AI agents actually work so that support teams can make better buying decisions.