Why fintech support breaks the usual AI playbook

Most "AI for customer service" advice is written for ecommerce or SaaS, where the worst case of a bad answer is a confused customer and a refund. Fintech doesn't get that grace.

I've spent the last few years putting AI agents on live support queues, and the fintech demos are the ones where I watch the buyer hold their breath. The reason is simple: the questions look easy ("did my payment go through?") but the cost of getting one wrong is regulatory. Tell a customer their transfer cleared when it didn't, confirm a card is safe when it's been compromised, or wander into anything that reads like financial advice, and you're not dealing with a support escalation anymore.

At the same time, fintech support teams are drowning in exactly the kind of repetitive volume AI is built for. Card activation, transaction status, KYC and verification chasers, statement requests, password and login help. These are the same five questions over and over, and they spike hard around paydays, month-end, and product launches. That's the tension: the volume screams "automate this," and the risk profile whispers "be careful."

Here's the thing I wish more people led with. The fix isn't a smarter model. It's a tighter scope and a harder set of guardrails. Once the boundaries are right, fintech is actually one of the better-fit verticals for AI support, because the high-volume questions are so repetitive and so well-documented in your own help center.

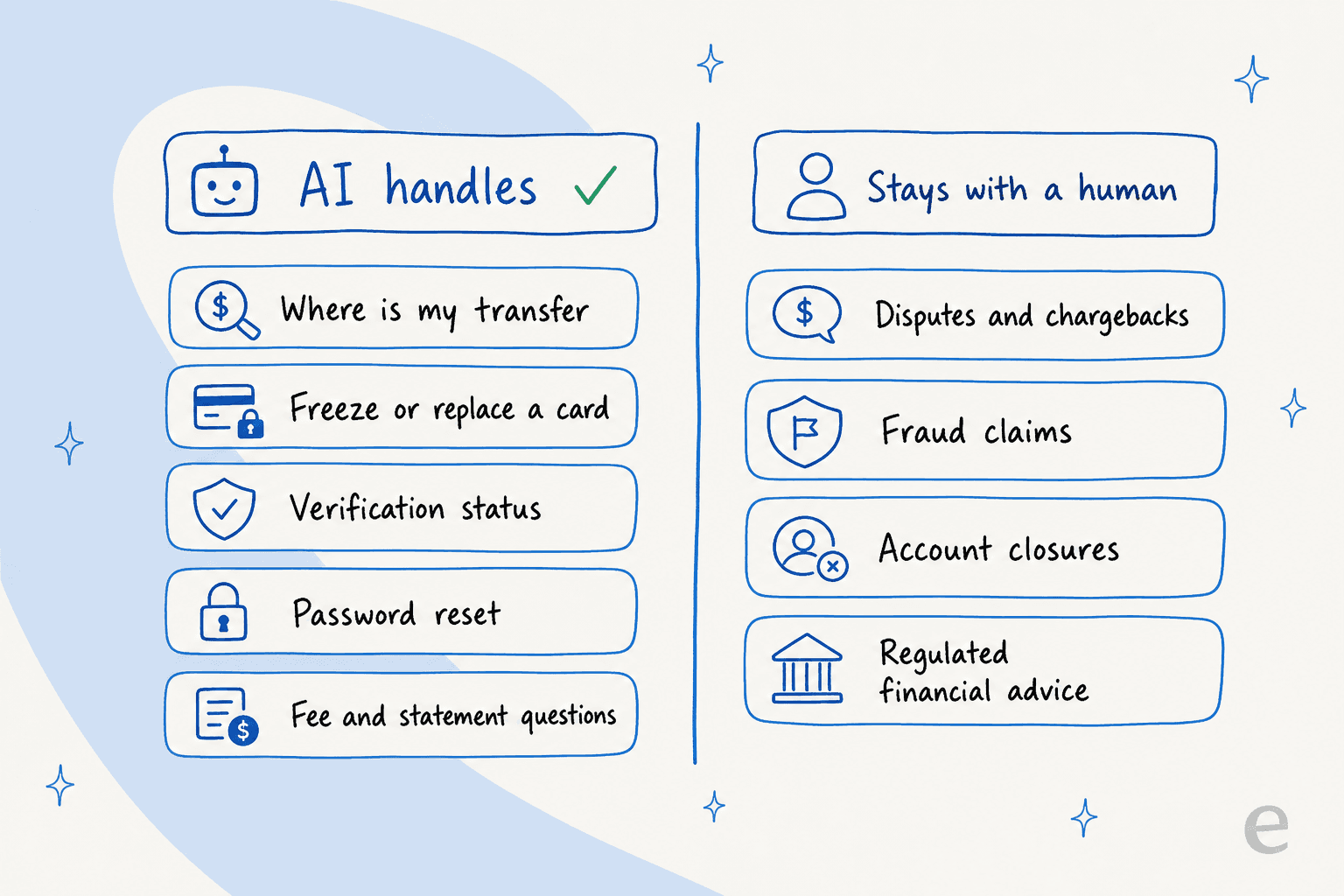

What AI customer service actually handles in fintech

Let me be concrete about where the line sits, because "AI handles support" is too vague to act on.

On the left side, the AI earns its keep. A good AI helpdesk agent can fully resolve transaction-status questions, card freeze and replacement flows, where-is-my-verification chasers, fee and statement queries, and the endless password and login resets, all by pulling the answer from your own help docs and past tickets rather than improvising. This is the same first-contact resolution work a tier-1 agent does, minus the wait time and the after-hours gap.

On the right side, the AI's job is to recognise the ticket and get out of the way. Disputes and chargebacks, fraud claims, account closures, and anything that crosses into regulated financial advice should route straight to a human with the context attached. The skill isn't answering these, it's reliably not trying to.

Two more roles matter beyond "resolve or escalate." The first is drafting: instead of auto-sending, the AI writes a suggested reply and leaves it as an internal note for an agent to approve. For a compliance-conscious team, this copilot mode is often where you start, because a human still presses send on everything. The second is triage: even on tickets it won't answer, the AI can tag, prioritise, and route, so a fraud claim never sits behind a stack of password resets.

The best part is that none of this requires ripping out your stack. eesel sits on top of the helpdesk you already run, so the AI works inside the same Zendesk or Freshdesk queue your agents live in.

The compliance bar: what to demand before connecting a single ticket

This is the section that actually decides whether AI customer service happens at your fintech company, so I'm going to be specific. In nearly every fintech evaluation I've been part of, the deal lives or dies on the security review, not the demo.

I've sat in calls where a buyer's first real question wasn't about accuracy at all. One Danish telematics team raised it bluntly: their tickets contain card numbers and passwords, so does all of that data stay inside their environment? A media company running about 1,000 tickets a week told us flat out that credit-card and PII redaction was the single thing standing between a trial and a contract. These aren't soft preferences. They're hard gates, and a vendor that fumbles them is done.

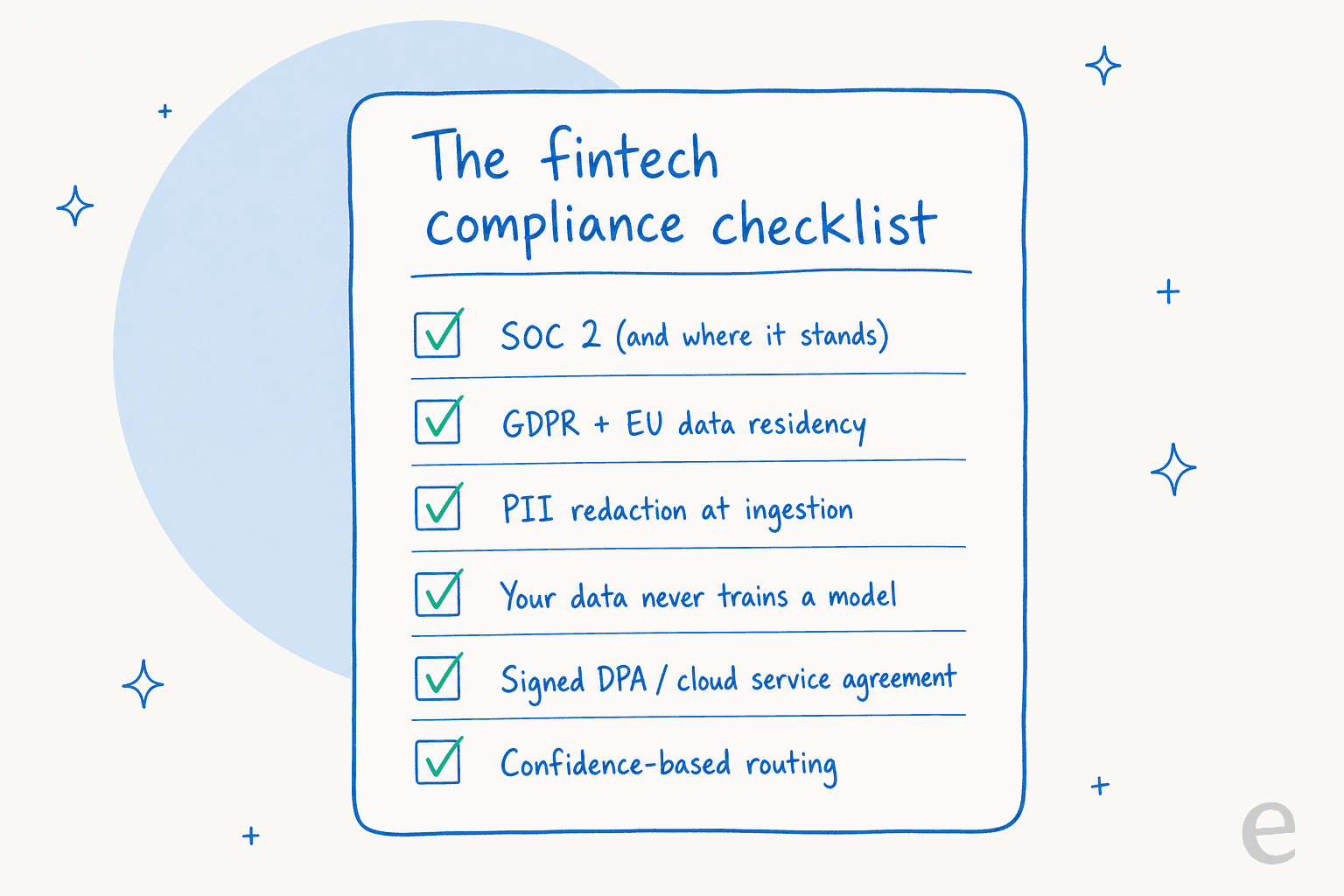

So here's the checklist I'd hand any fintech support leader before they connect a ticket.

| What to demand | Why it matters for fintech | The question to ask |

|---|---|---|

| SOC 2 status | The baseline security attestation most fintech procurement teams require | "Are you SOC 2 Type II certified, in progress, or neither? Can I see the report under NDA?" |

| GDPR + data residency | EU customer data often can't leave the region | "Are you GDPR compliant, and can you host my data in the EU?" |

| PII redaction | Tickets are full of card numbers, SSNs, and account details | "Do you strip PII before it reaches the model, and when does that happen?" |

| No model training on your data | Your customers' financial data must not leak into a shared model | "Is my data ever used to train your models, ever?" |

| DPA / cloud service agreement | Your legal and security teams need something to sign | "Can we sign a DPA and a formal security agreement?" |

| Confidence-based routing | Stops the AI guessing on questions it shouldn't touch | "What happens when the AI isn't sure?" |

For what it's worth, here's where eesel lands on that list, because I'd rather show you than pitch you. eesel's security page states that your data never trains its models, full stop, and that each workspace is fully isolated so nothing crosses between customers. Optional PII redaction strips card numbers, emails, phone numbers, SSNs, and API keys at ingestion, before the data ever reaches an AI provider or even eesel's own search index. On certifications, eesel is GDPR and CCPA compliant with EU hosting available on request, data is encrypted with AES-256 at rest and TLS 1.2+ in transit, and SOC 2 Type II is in progress with continuous monitoring (you can see the live status on the Vanta trust center). Deletion requests are honoured within 60 days, and enterprise plans can sign a Common Paper DPA and a cloud service agreement.

I'll be straight about the one place I'd push back if I were buying: SOC 2 Type II is still underway rather than certified, and if your procurement team treats the certificate as a non-negotiable gate today, that's a real conversation to have up front rather than at contract stage. A vendor who tells you that honestly is worth more than one who waves it away. (For comparison on how the bigger platforms handle this, our deep dive on Freshdesk security and SOC 2 is a useful reference point.)

Accuracy is the other half: stopping the confident wrong answer

Compliance keeps your data safe. Accuracy keeps your answers safe. They're different problems, and fintech needs both.

The failure mode I worry about most isn't an AI that says "I don't know." It's an AI that's confidently wrong, the bot that cheerfully tells a customer their dispute is resolved when it isn't. I've watched a confident-sounding bot quietly hand out wrong answers, and that experience is exactly why every eesel rollout is built around two ideas.

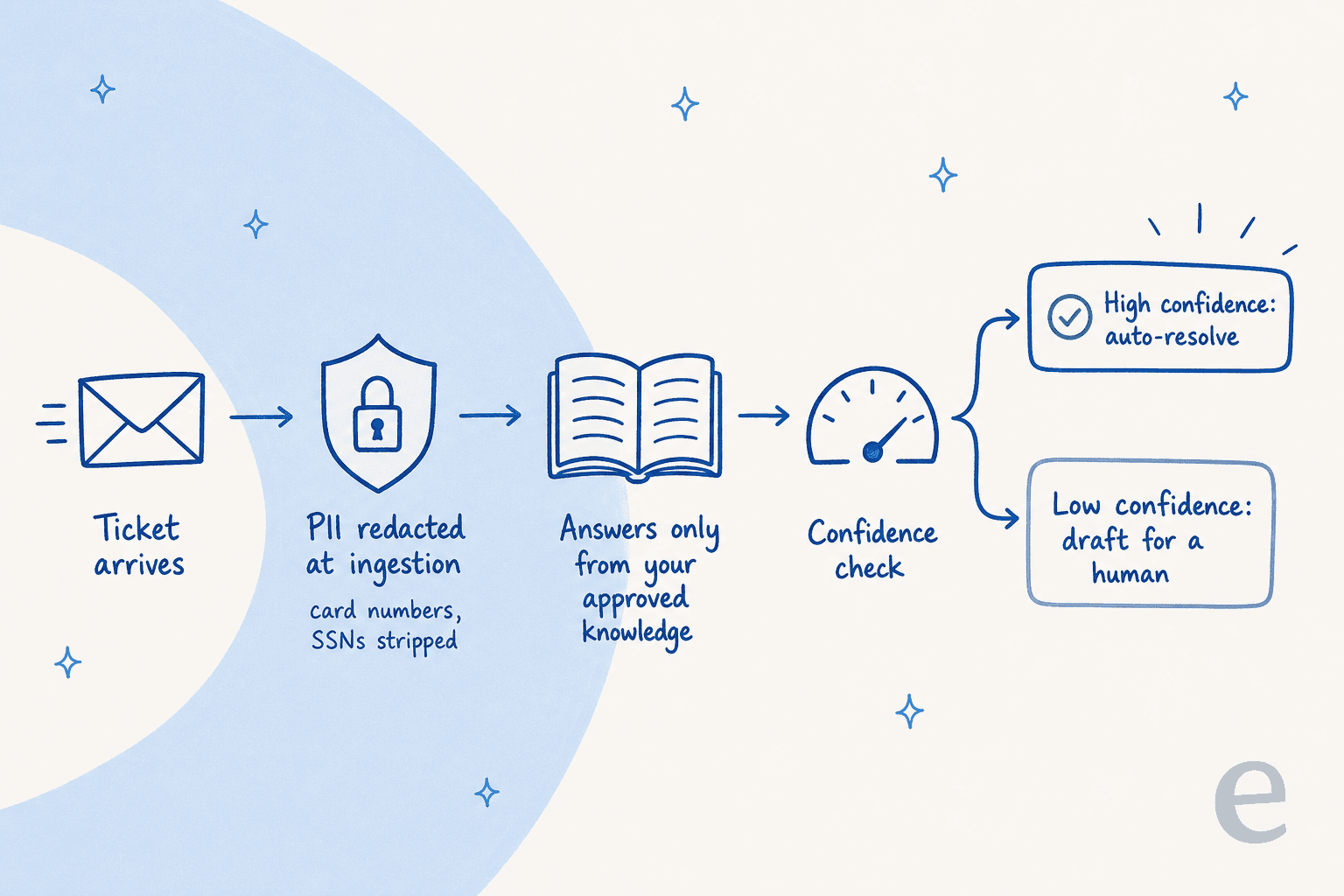

The first is grounding. The AI answers from your help center and your solved tickets, not from whatever it absorbed in training. If the answer isn't in your knowledge, it doesn't get invented. This is the retrieval-based approach, and it's the single biggest factor in why a support bot answers correctly or doesn't.

The second is confidence-based routing. Every potential answer carries a confidence level, and you set the threshold. Below it, the AI doesn't reply live, it drafts for a human or escalates. Here's how that whole flow looks for a single fintech ticket:

The reason this matters so much for fintech is that you get to decide the boundary, ticket type by ticket type, rather than flipping one big "AI on" switch. Exclude dispute tickets entirely. Let the AI resolve transaction-status questions on its own but only draft on anything mentioning fraud. That granularity is the difference between an AI you trust with money questions and one you don't.

And before any of it goes live, you simulate. eesel runs the agent against thousands of your real historical tickets and shows you, by theme, what it would have answered and how accurate it would have been. You find the gaps and fill them while a customer is nowhere near the conversation. In one real-traffic trial on a retailer's live queue, that simulation surfaced 93% triage accuracy and 100% spam detection before launch, the kind of number you want to see on a spreadsheet, not discover in production.

Once it's live, every action the AI takes is logged and reportable, which is its own kind of compliance feature.

The payoff, when the scope and guardrails are right, is real. One gig-economy analytics company on Zendesk put it plainly:

"In the first month, eesel is resolving 73% of our tier 1 requests. eesel offers easy Zendesk implementation and setup. Our team implemented and achieved results quickly during our 7-day trial."

Kim Simpson, Gridwise (eesel AI helpdesk agent)

That 73% wasn't from a clever model. It was from a well-scoped agent grounded in their own tickets, which is the whole point.

What AI customer service for fintech actually costs

Pricing is where a lot of fintech AI deals quietly fall apart, because the model matters more than the sticker.

The trap is per-resolution pricing. The better your AI gets, the bigger your bill, which is a strange thing to be penalised for. eesel uses straight usage-based pricing: $0.40 per ticket handled, no per-seat fees, no platform fee on the self-serve plan, and no monthly minimum. A ticket is one task no matter how many back-and-forth messages it takes, and you're never charged for tickets your human agents handle.

| Tickets routed to AI / month | Monthly cost |

|---|---|

| 100 | $40 |

| 500 | $200 |

| 1,000 | $400 |

| 2,500 | $1,000 |

Here's a worked example for a mid-size fintech team. Say you get 2,500 support tickets a month, and after scoping, you're comfortable letting AI handle the 60% that are low-risk tier-1 (status checks, card flows, password resets). That's 1,500 tickets to AI at $0.40 each, so $600 a month, with the remaining 1,000 sensitive tickets staying with your team. Compare that to the fully loaded cost of the agent hours those 1,500 repetitive tickets would otherwise eat, and the math gets obvious fast. If you want to run that comparison properly, we broke it down in AI agent vs human agent cost and how much AI can save in support.

One more thing fintech finance teams appreciate: you can set a monthly spend cap (it defaults to $250), get alerts at 50, 75, and 100% of it, and the agents auto-pause at the limit. No surprise invoice, which matters when your CFO is also your security reviewer.

Try eesel for fintech support

If you're weighing AI customer service for a fintech or financial-services team, eesel is built for exactly the cautious, scope-it-first approach this guide argues for. It connects to the helpdesk you already run (Zendesk, Freshdesk, HubSpot, Gorgias, Front, Salesforce, and 80+ languages out of the box), learns from your past tickets and help docs, redacts PII before anything reaches a model, and lets you simulate against your real ticket history before a single customer sees an AI reply.

The one differentiator I'd point to for this vertical: gradual, ticket-type-by-ticket-type autonomy with confidence-based routing, so you can let AI own status checks while keeping every dispute and fraud claim with a human. You can start free with $50 of usage and no credit card, run a simulation on your own tickets, and see the accuracy before you commit. Try eesel or read the full customer service AI comparison if you're still shortlisting.

Frequently Asked Questions

What is AI customer service for fintech?

Is AI customer service secure enough for financial services?

How much does AI customer service for fintech cost?

Can AI handle compliance-sensitive tickets like disputes or fraud?

How do I stop an AI support agent from giving wrong answers?

What helpdesks does AI customer service for fintech work with?

How long does it take to get AI customer service live for a fintech team?

Article by

Alicia Kirana Utomo

Kira is a writer at eesel AI with a Computer Science background and over a year of hands-on experience evaluating AI-powered customer service tools. She focuses on breaking down how helpdesk platforms and AI agents actually work so that support teams can make better buying decisions.