What an "AI chatbot for fintech" actually means

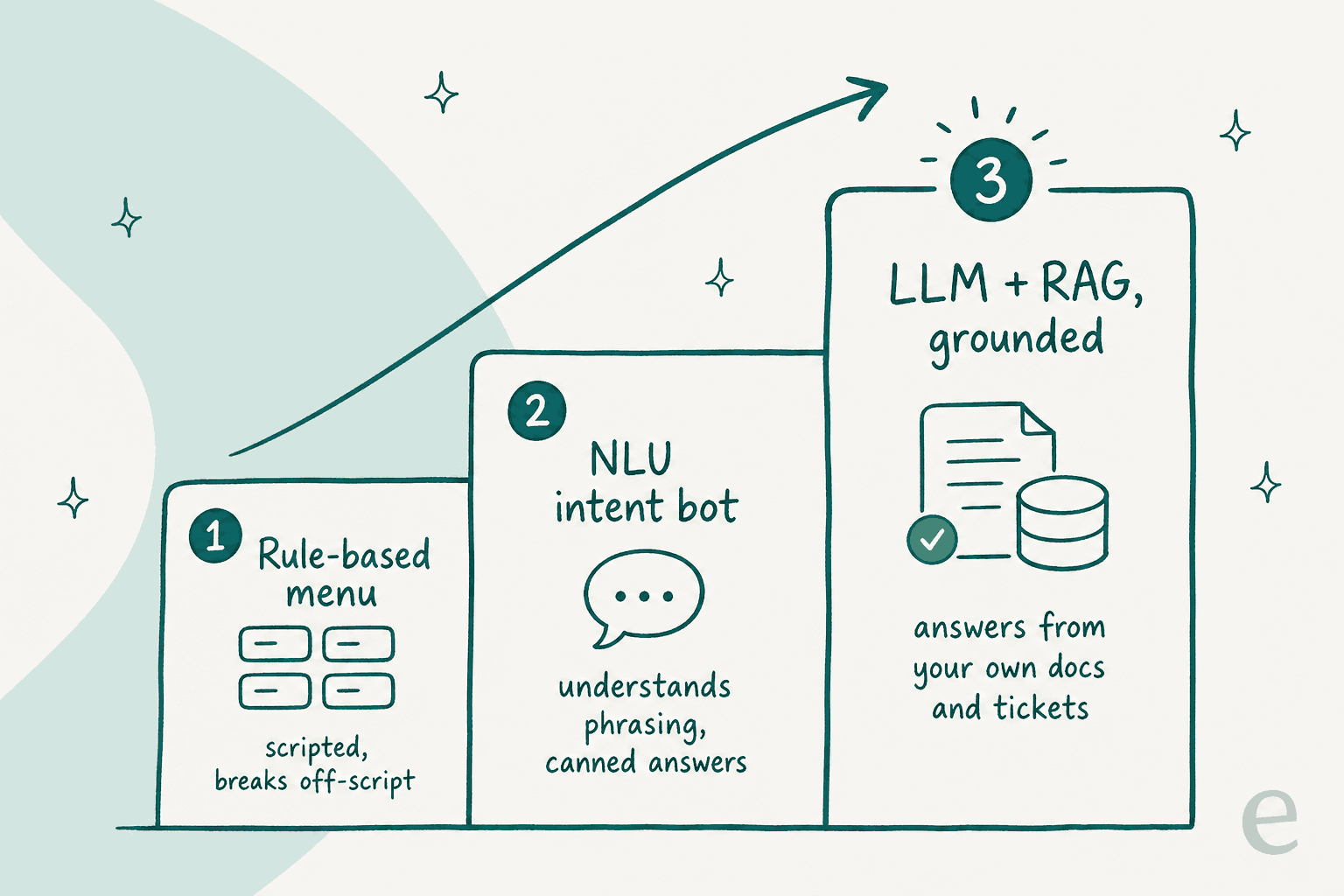

I build the integrations that plug support AI into helpdesks for a living, so let me be precise about the ladder, because a fintech team buying at the wrong rung is where most of the horror stories start. The phrase "AI chatbot" covers three very different things.

The bottom rung is the rule-based menu: scripted buttons and decision trees. It is predictable, which regulated teams like, but it breaks the moment a customer types something off-script, and fintech customers always do. The middle rung is the NLU intent bot, which understands phrasing better but still hands back canned, pre-written answers. The top rung is an LLM grounded with RAG, which reads your actual help center and ticket history and writes a real answer to the specific question. That is the rung this whole post is about, and it is the one worth the compliance homework. If you want the plain-English version of that acronym, we wrote up what RAG means.

The mistake I see most often is a fintech team buying a rule-based tool, calling it "AI" internally, and then being surprised when deflection stalls at 10%. The gap between a scripted bot and a real AI agent is the difference between a phone tree and a teammate.

What fintech teams actually use them for

The honest scope is narrower than the sales decks suggest, and that is a good thing. The tier-1 tickets that dominate a fintech queue are repetitive and answerable from docs, which is exactly what support-ticket automation is good at:

- Account and transaction questions. "Why is this pending?", "What's this charge?", "When does my transfer clear?" These are high-volume, low-risk, and mostly answerable from your own knowledge base.

- Payment failures and card actions. Declined cards, failed direct debits, freezing a lost card. The bot can explain the why and walk the customer to the fix, or trigger the action and confirm it.

- KYC and onboarding status. "Where's my verification?", "What documents do you need?" Verification is the single most-asked question at most fintechs, and it is pure deflection gold.

- Fees, limits, and plan questions. The stuff buried three clicks deep in your help center that customers would rather ask than hunt for.

Notice what is not on that list: disputes, chargebacks, fraud, closing accounts, or anything resembling financial advice. Those get recognised and escalated, never resolved by the bot alone. Knowing where the line sits is most of the job, and it is the same discipline behind good ticket triage generally.

Why fintech is different: a wrong answer costs more

In most support queues, a bad bot answer means a frustrated customer and a follow-up ticket. In fintech, a bad answer can mean a mis-stated fee, a confirmed-but-wrong balance, or a dispute the bot failed to recognise, and any of those can put you on the wrong side of consumer-protection rules. The CFPB's chatbot report is worth reading precisely because it treats a bad bot as a legal exposure, not a UX nitpick.

That raises the stakes on two things most buyers underweight. The first is hallucination: a general-purpose model will happily invent a plausible-sounding fee structure if you let it answer ungrounded. The fix is grounding plus refusal, and it is worth understanding why chatbots answer incorrectly, one of the most common AI chatbot problems, before you trust one with money questions.

The second is data handling. Fintech tickets are full of the exact data you least want a model to memorise. This is the objection that gates most fintech deals, and it is a hard blocker, not a soft concern. One buyer I think about often is a fintech-adjacent telematics team whose security review flagged that tickets routinely contain card numbers and passwords, and who would not start a trial until they were sure that data stayed inside their environment. The reassuring answer, and the one that closed it, is that a well-built system looks at the type of question and the style of the agent response, not the raw PII, with redaction and custom retention for finance clients. If your vendor cannot explain that in one sentence, that is your answer.

What real fintech teams say

The most credible fintech signal I have is from a payments company that put our AI Copilot over their internal knowledge and measured the result:

"In a business where transactions need to be processed as quickly as possible, every second counts. With eesel, we can find specific answers to questions extremely fast. We can onboard new employees very quickly and have seen up to 80% time savings."

Chief Innovation Officer, payments/fintech company

That is the upside when grounding is done right: fast, specific answers pulled from approved knowledge. But the objection that comes up in nearly every fintech evaluation is control. Teams do not want a bot that answers everything, they want a bot that answers only what it is sure of. One CX lead put the trust problem more sharply than any analyst report I have read:

"The AI will never be able to answer 100% of the questions, but if it tries and just answers 'sorry I don't know this,' I cannot go and check all my 7,000 tickets to see if the AI actually made a good answer. I need an AI who is only handling the tickets that it's confident to handle and all the other ones, leave them alone."

CX lead, high-volume consumer brand (~7,000 tickets/month)

That is the whole design brief for a fintech bot in two sentences. Confidence is not a nice-to-have, it is the feature.

What makes a fintech bot actually work

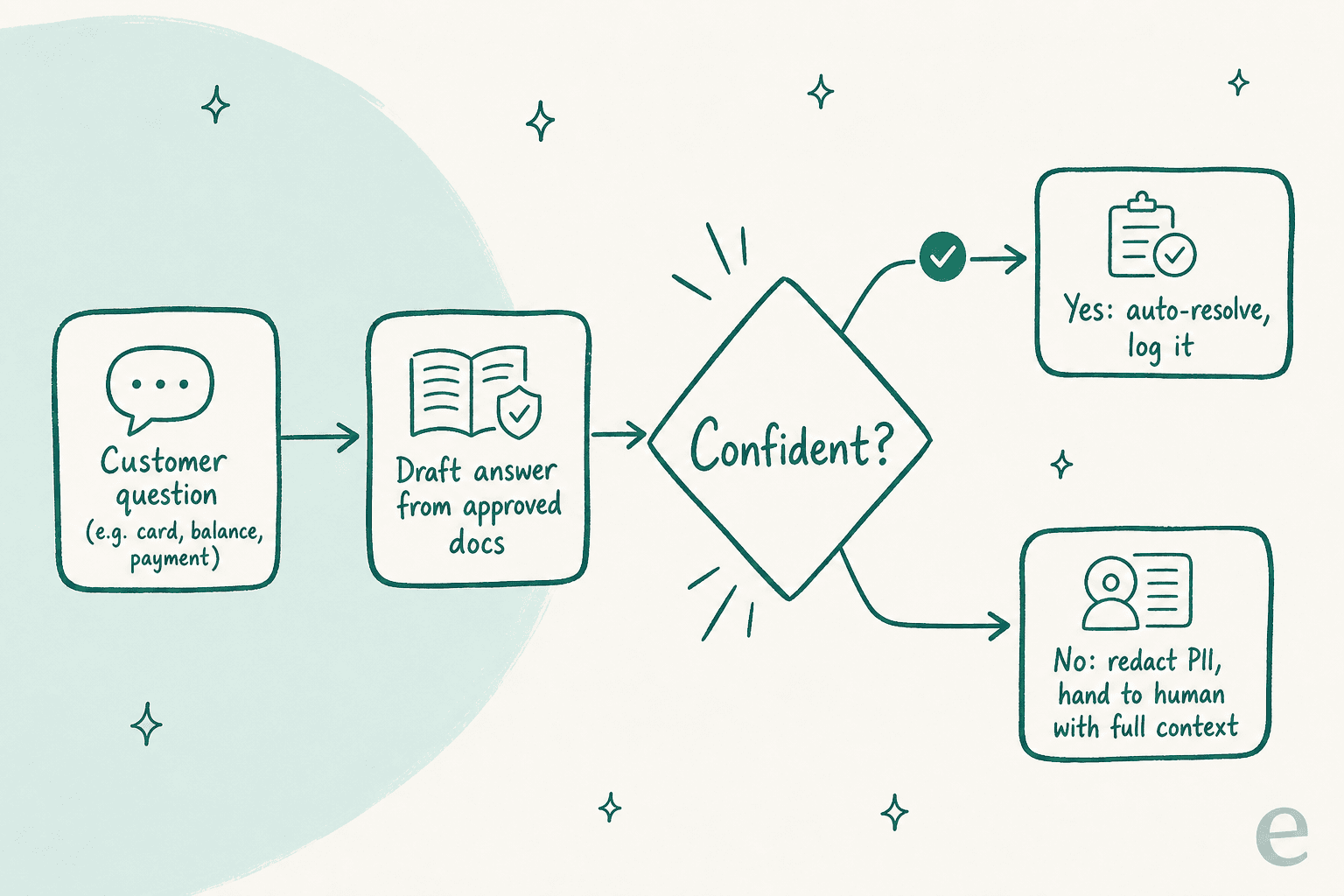

Here is the flow a grounded, confidence-gated bot follows on a single ticket. It is less "AI magic" and more "a careful teammate who knows when to tap out".

The mechanics that matter, in order of how much they protect you:

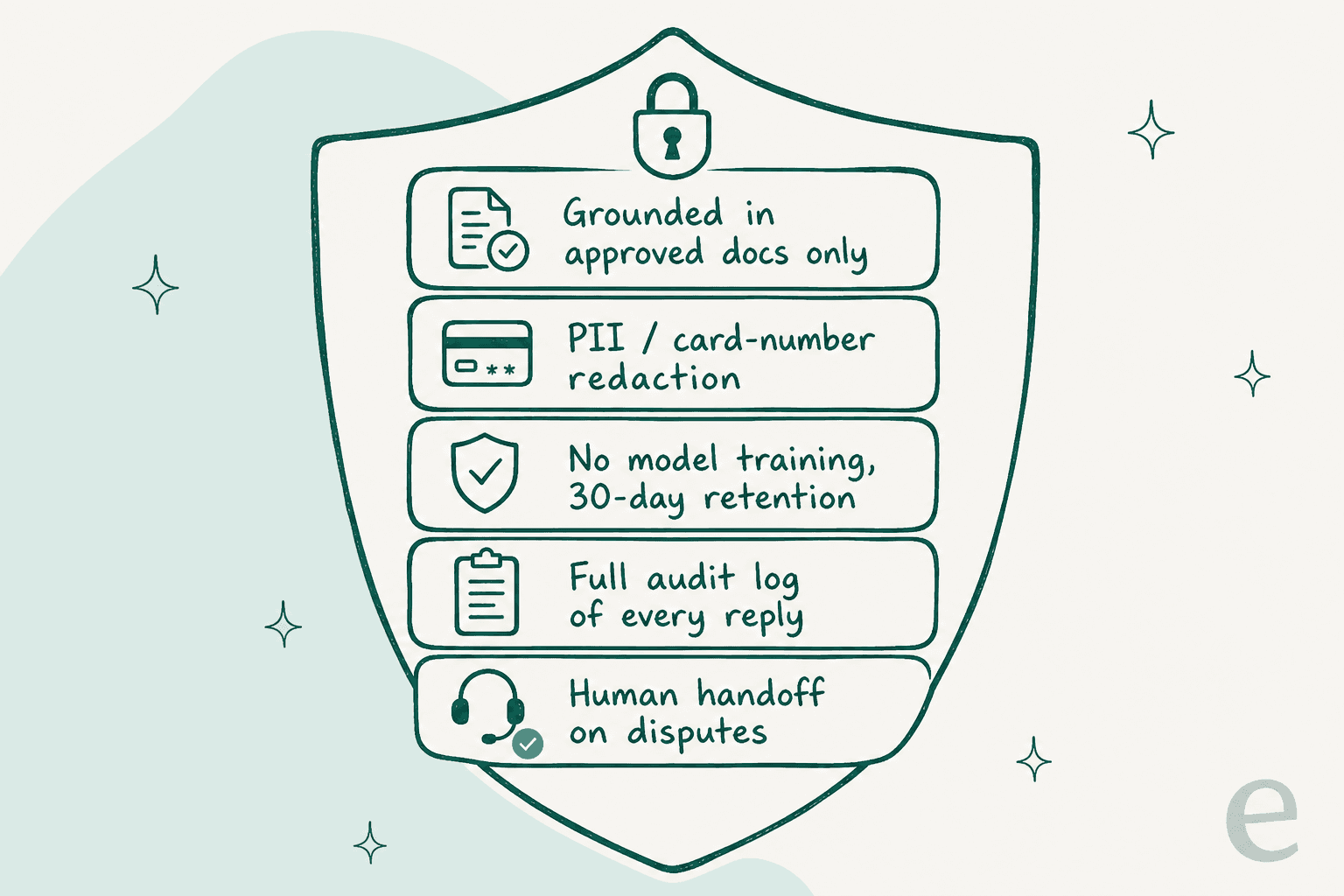

- Grounding in approved docs only. The bot answers from your help center, policies, and past resolved tickets, and refuses when it has nothing to cite. This is the single biggest lever on accuracy, and it is why AI knowledge management is the real prerequisite, not the model choice.

- Confidence-based routing. Below a threshold, the bot does not guess, it routes to a human with the full context. This is the control the CX lead above was asking for, and the thing that turns "scary AI" into "safe AI".

- PII redaction. Card numbers and other sensitive fields get stripped before anything is processed, with retention controls that fit a finance compliance posture.

- A clean human handoff. Any dispute, fraud flag, or account action goes to a person, fast, with everything the bot already gathered. Good AI escalation is what keeps the bot on the right side of the compliance line.

Wrap all of that in an audit trail and the picture gets a lot more defensible.

On the data question specifically, the answers a fintech security team needs are concrete: your data does not train the underlying models, the model providers retain data for a short window for abuse monitoring only, and everything is siloed per account, with PII reduction and EU data residency available. Those are the details that move a deal from "interesting" to "approved", and they live on our security page.

How to deploy one without getting burned

The failure mode I have watched teams walk into is switching the bot on against live customers and hoping. In fintech, "hope" is not a deployment strategy. Here is the sequence I would actually run:

- Point it at your knowledge first. Connect your help center and resolved tickets before anything else. A bot with thin knowledge is a bot that hallucinates, and disorganised docs are the real bottleneck, not the model.

- Simulate against your history. Run the bot over thousands of your real past tickets in a sandbox and read what it would have said, before a customer ever sees it. This is the step that catches the fee it would have mis-explained. It is the core of how eesel AI is designed to work, and I do not know why anyone ships a fintech bot without it.

- Start narrow, on high-confidence topics. Let it own KYC status and "where's my transfer" first. Exclude disputes and account actions entirely at launch.

- Watch the numbers, then widen. Track deflection rate and first-contact resolution, read the escalations, and only expand scope once the confidence threshold is earning its keep.

One more thing that catches fintech buyers off guard: pricing units. A per-resolution or per-message model creates back-and-forth anxiety, because every follow-up feels like it costs money. I would look hard at what you are actually billed for. eesel AI is pay-as-you-go pricing at about $0.40 per ticket with no platform fee, which is the kind of predictability a finance team can actually forecast. It helps to know how chatbot cost is usually structured, and how it stacks against the cost of a human agent on the same tickets.

Try eesel AI for fintech support

If you run support at a fintech and the compliance story is what has kept you off AI, that is the exact problem eesel AI is built for. It plugs into the helpdesk you already use, grounds every answer in your own knowledge, routes anything it is not confident about to a human, and, most importantly, lets you simulate the whole thing against your real past tickets before a single customer is exposed to it. No training data leaves your account, and PII redaction plus EU residency are there for the security review.

It is free to try, and you can watch it work on your own historical tickets before you commit to anything. For the wider picture, our overview of AI in customer service, the vertical guide to customer service for fintech, and the deeper cut on conversational AI for finance are good next reads.

Frequently Asked Questions

What is an AI chatbot for fintech?

Is an AI chatbot for fintech safe and compliant?

How much does an AI chatbot for fintech cost?

Can an AI chatbot for fintech handle disputes and fraud?

What is the best AI chatbot for a fintech support team?

Article by

Rama Adi Nugraha

Rama is a software engineer at eesel AI with two years of experience writing about B2B SaaS, AI tools, and customer support technology. Based in Bali, Indonesia, he brings a developer's perspective to product comparisons — cutting through marketing copy to what the integrations and APIs actually do.